10-Year Treasury Yield Interpretation: Monthly/Secular Perspective Overview | “Filling the Gaps” with CMT

I begin each year by reviewing the long-term technical position and behavior of the “big four”: 10-year yield, S&P 500 ($SPX), commodities, and the U.S. dollar. I believe that interest rates generally drive economic and market cycles, especially in credit-dependent/leveraged systems. And by profession I am an interest rate/credit portfolio manager, strategist and trader, so I always start there.

Of course, a macro perspective won’t help you with short-term trading, but anything that helps you understand the ebbs and flows and interconnectedness of the markets is helpful. More importantly, recognizing markets that are aligned to important macro changes can be invaluable, especially from a risk management perspective.

Because the best technical analysis is fractal, the same techniques used to describe macro ebbs and flows can often be translated to shorter time periods. For the first 20 years of my trading career, I manually managed the Big 4 and a few other markets (gold, oil, two-year Treasury bonds, etc.), updating prices and previous price changes every hour. hour. In doing so, I learned a lot about market interactions and interrelationships.

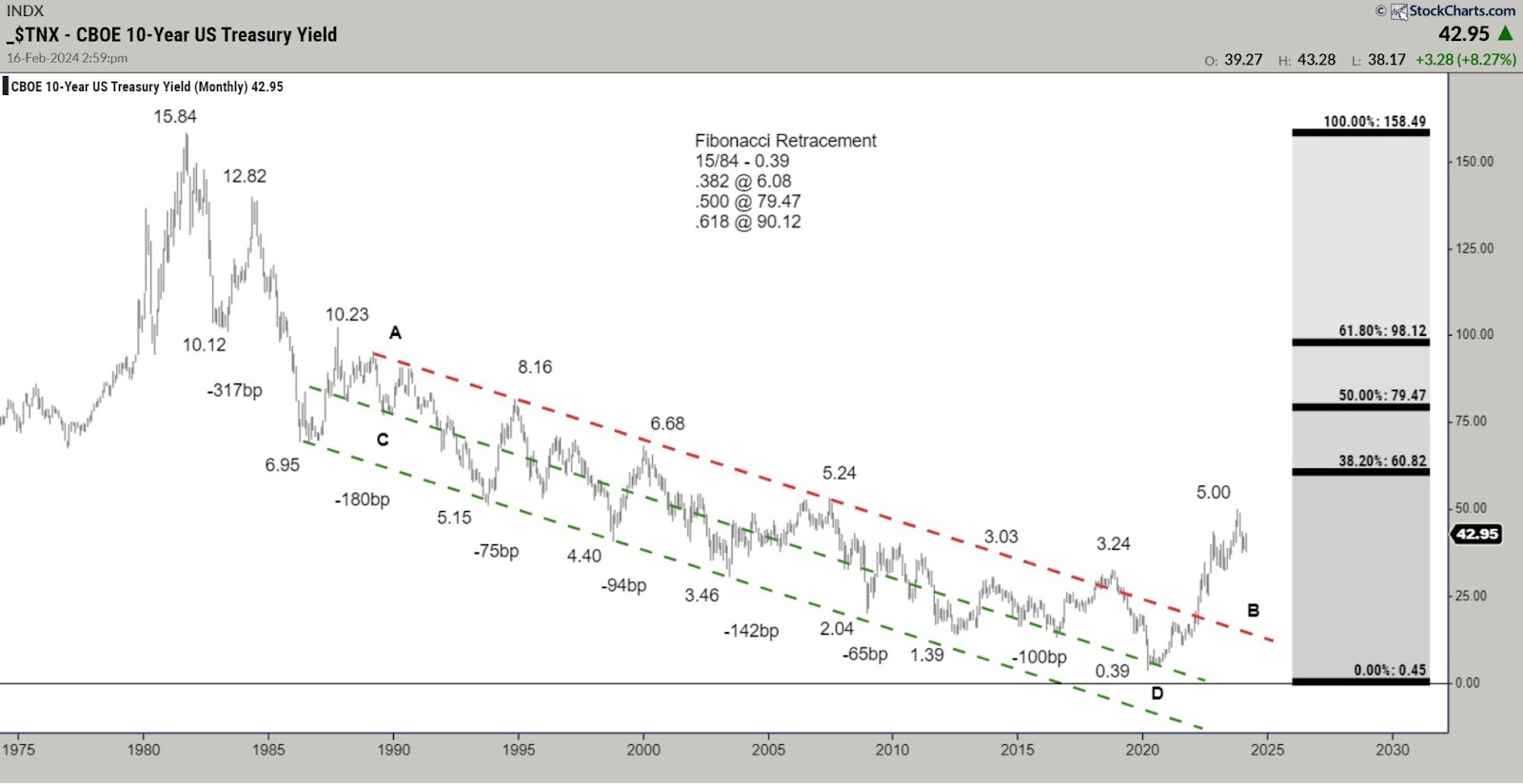

Monthly 10-Year Treasury Bond Yield

Chart 1. Monthly chart of 10-year Treasury yields. Over the past 40 years, bond yields have consistently and reliably made lower highs and lower lows. The entire bull market was defined by a broad downward channel (A–B, C–D). The AB downtrend line represents the “demand stride”, i.e. the area where buyers are consistently present, while the CD line represents the “overbought line”, i.e. the area where supplies or sellers are consistently present.

Take notes. Falling bond yields are synonymous with rising bond prices. In other words, a downward trend in yields = a bull market for bonds.

Since 2012 there have been growing signs that the long-term downward trend is aging. Four things stood out.

- Repeated failure to enter the oversold line (CD).

- Each push toward a new yield low has flattened the decline by only about 100 bps.

- In 2018, it soared to 3.24%, weakening the downward trend of the first AB.

- In March 2020, bonds pushed into an area near the center of the channel and failed to push past the midline to the overbought line (CD). This change in behavior strongly suggested that demand was exhausting. Several notable behavioral changes strongly suggested that the 40-year downward trend was at risk of ending.

AB A clear breakout and acceleration above the downtrend shifted the long-term trend from bullish to neutral. A move above the 3.24% November 2018 pivot along with previous behavioral changes would likely signal the start of a long-term bear market, but a higher low (probably forming in 2024) would be needed to complete/confirm such a change. .

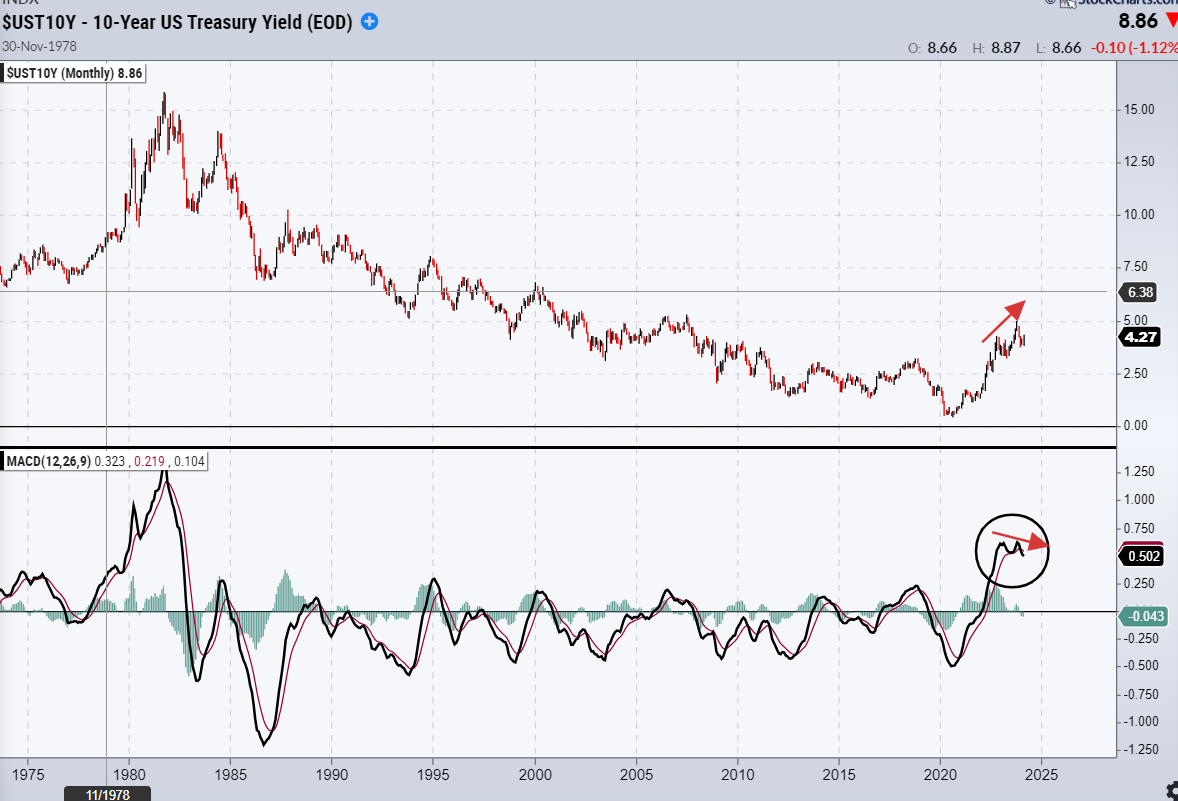

Please note additional changes in behavior. The 459bps move from 0.39% to 4.98% represents the single largest bearish move since the bull market began in September 1981, with the MACD oscillator Returns far exceeded the highest levels of the entire bull market.

10 Year Monthly Returns Using MACD

After hitting the most overbought reading since the 1980s, the oscillator is attempting a rollover and is showing a small negative divergence (yields are low and prices are high). Although this is not a definitive ruling, it suggests the possibility of a meaningful change of direction.

Chart 2. Monthly chart of 10-year Treasury yields.

10 Year Weekly Returns

The following charts cover the weekly perspective, 5-year and 10-year charts, and the yield curve.

Chart 3. Weekly chart of 10-year returns.

Here are some key basics regarding interest rates:

- A macro characteristic of the 40-year bull market was the continued decline in inflation rates. If that is changing (and I believe it has been), the long-term bond trend is likely to change as well.

- As inflation trends change, the negative correlation between bonds and stocks that drives 60/40 allocations and risk parity investing is likely to reverse and become a positive correlation. That is, bonds and stocks will rise and fall together during periods of no depression or economic hardship, destroying the benefits of diversification. This has been the historical norm, and the market is expected to gradually move in that direction.

- Caveat: Quantitative easing has taken the value proposition out of bonds. As stocks begin to fall in 2022, bonds couldn’t do it Provides a safe haven. This was already too expensive, especially with the Federal Reserve aggressively tightening monetary policy. That is no longer the case. Bonds are still expensive, but they can again provide a tactical hedge if the asset or the economy weakens sharply.

- At first glance, this may seem strange from the change in correlation discussed above, but it is the difference between the middle wave and the middle wave.

- Most real bond rallies stem from crises that create quality-seeking crises. In overly financialized and leveraged economies, rising interest rates often break the weakest link in the economic chain, triggering new crises and subsequent quality-oriented rallies. Although there is little evidence of a systemic crisis, the lagged effects of sharp interest rate increases in an overly financialized system should be kept in mind.

conclusion

There is still more work to be done to see trends change, but we believe bond trends are finally changing as the world moves from the deflationary backdrop of the past few decades to an inflationary backdrop. I would be a much better seller on rally and bearish technical setups from a weekly/mid-week perspective.

disclaimer: Shared content and published charts are for informational and educational purposes only. CMT Association does not provide this information, and this information should not be understood or construed as financial advice or investment recommendations. The information provided is not a substitute for the advice of an investment professional. CMT Association will not be liable for any financial loss or damage that may occur to the audience.

Good deal.

Stuart Taylor, CMT

Certified Market Technician

Stewart Taylor retired from Eaton Vance Management in January 2020 after a 40-year career in U.S. fixed income with a focus on technical analysis and relative value investing. He joined Eaton Vance in 2005 as a senior trader on the investment grade fixed income team. During his tenure, he served as a portfolio manager for institutional separate accounts and mutual funds, managed the team’s inflation assets, and served for a time as the team’s strategist. Value, economic positioning. From 1992 to 2005, he provided private investment and trading advice to institutional buy-sides, broker-dealers, and hedge funds. Learn more