Occidental Petroleum’s Diverse Strategy Could Pay Off (NYSE:OXY)

")

Nilubiclone

Occidental Petroleum (New York Stock Exchange: Oxy) is making progress in establishing itself as a carbon-friendly oil producer as the company further develops full cycle well remediation through CO2 direct air capture and EOR for well remediation. With oil The industry faces a stagnant crude oil market in eFY24 along with easing production-related inflationary pressures. I believe Oxy is well positioned to optimize well production through CO2 injection and asset clustering strategies. I believe that with the planned deleveraging program, reinstated share buyback program following the anticipated CrownRock acquisition, and enhanced oil recovery program, Oxy will be a strong turnaround and growth investment for years to come. I give OXY stock a Buy recommendation with a target price of $90.10 per share for 6.08x eFY25 EV/aEBITDA.

operate

Like many IOCs, Oxy is well positioned to navigate these challenges effectively. Concentrating production on long-term cyclical assets is expected to flatten the oil market in eFY24. In its fourth quarter 2023 earnings call, management identified that it will focus on strengthening its move to add a second drillship in the Gulf of Mexico to further develop its offshore assets. With WTI prices currently hovering above $80 per barrel, we believe this long-cycle strategy will alleviate some of the capital intensity seen in near-term unconventional production. Management forecast a $320 million decrease in capital spending for near-term and exploration in eFY24 and a $480 million increase in capital budget for mid-cycle investments. Management expects the production split to be 65/35 shale/offshore upon completion of the CrownRock acquisition within 24 hours, with a balanced portfolio.

Oxy has spent a lot of time strengthening its assets over the past three years to strengthen its long-term strategy. As of FY23, the company has nearly doubled its proven undeveloped reserves since 2020 to 1,232 MMboe, and its developed proven reserves have increased to 2,750 MMboe, bringing its total proven reserves to 4 Bboe. I believe that through strategic acquisitions, Oxy is working to strengthen its valuation on a reserves basis while maintaining discipline in production growth. For eFY24, management expects total production to increase by 2%. This strategy will benefit Oxy in the long run as the company manages and top-rates its assets for a better pricing environment. This can be seen through the company’s all-in reserve replacement of 137% for FY23. Management expects to invest $5.8 billion to $6 billion in fiscal 2024, with a focus on mid-cycle assets across its Energy and Chemicals businesses. In addition to this, Oxy plans to invest an additional $600 million in low-carbon ventures and may receive additional investment from BlackRock.

Oxy experienced production from its Rockies and DJ Basin assets, with Permian production steady in the fourth quarter of 2023. Assets in the Rockies and Al Hosn will be the primary focus of production growth in eFY24 as the company secures Tier 1 assets in the Permian. I believe Oxy’s plan to focus on lower-tier wells could create a near-term margin headwind. However, this strategy will preserve the company’s upstream assets for a stronger oil market when production capacity can be better realized.

Permian Basin management expects production rates to remain maintained as it navigates the current oil price cycle. Oxy is currently working to implement EOR and direct air capture investments while also increasing gas processing capacity with new facilities in the Permian Basin. Management expects the DAC facility to come online in mid-2025, hinting that EOR and direct air capture will likely come online in 2026.

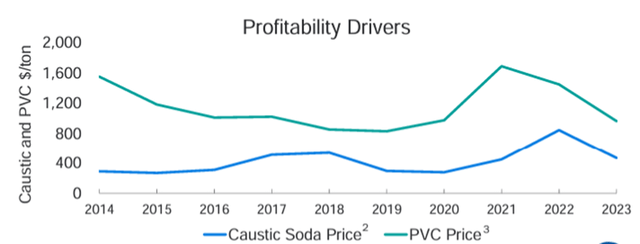

On the chemicals side of the business, management expects near-term headwinds for PVC and caustics as pricing pressures from China remain unfavorable. Management expects OxyChem to generate $1-1.2 billion in EBT in eFY24. Management expects to invest $700 million in its chemicals business for the Battleground expansion and plant improvement project. Management expects construction of the Battle Ground facility to be completed by mid-2026. Once completed, the combined EBITDA impact of the new facility and plant improvement project will add 300 to 400 mm per year.

Oxy Investor Presentation

Financial forecasts show that Oxy faces a relatively depressed market in the O&G sector as the global economy fluctuates between growth and recession.

corporate report

Using strip prices published by CME as a guide, we expect oil prices to average the low 70s to low 80s by eFY24 and decline to around $75 per barrel by eFY25. We also expect natural gas prices to recover modestly over the next few years as domestic dry gas production stagnates. I believe Oxy will continue to increase production to meet the growing demand for oil. My forecast for eFY25 includes an additional 170 Mbbl/d from the CrownRock acquisition.

corporate report

For eFY24, slight margin expansion is expected as management guides lower operating costs per barrel for the next fiscal year. However, margins are expected to contract slightly year-on-year in eFY25 due to expectations of increased drilling activity and higher midstream costs.

Despite my optimistic tone, there may be certain risks to the downside that are worth considering. Oxy’s full cycle CCUS project is still several years away and may not achieve the recovery rates expected. Management also expects BlackRock to provide additional funding for a second DAC facility in Texas. BlackRock is moving away from the ESG label and has since crashed its ESG mutual fund. As more states tackle ESG-focused investing, raising external funds may not be as simple as it used to be.

Valuation and shareholder value

corporate report

OXY stock currently trades at a slight discount to its IOC peers at 5.90x EV/aEBITDA. I believe OXY stock holds a lot of hidden value that will be unlocked as the company moves toward CCUS. Since the company’s net debt far exceeds peer domestic IOCs at 1.43x net debt/aEBITDA, we believe the company needs to take some steps to shrink its balance sheet before it can achieve a higher equity premium.

corporate report

We believe the company will have the capital flexibility to do so, particularly as management scales back its share repurchase program pending the closure of CrownRock. This should free up additional capital to service debt while maintaining the increased payout ratio of $0.88 per share. Considering multiple scenarios for OXY, we believe the stock could experience some margin expansion over the next few years as the company cleans up its capital structure and moves toward decarbonization of its oil production process. I value OXY stock at $90.10 per share with a 6.08x eFY25 EV/aEBITDA and provide a Buy recommendation.

corporate report

I believe oil prices would need to rise into the upper $80-90/bbl range for OXY stock to reach a blue sky scenario. This is likely to happen as OPEC+ maintains production cuts alongside rising demand forecasts. In the target scenario, oil is priced at the current strip price. A gray sky scenario would suggest more price headwinds, putting oil prices in the low $70s.

")