Confirm: More Room for Growth in Favorable BNPL Environment (NASDAQ:AFRM)

")

Hapaapapa

Affirm Holdings Co., Ltd.NASDAQ:AFRM) recently announced its third quarter 2024 results, showing notable growth in GMV and revenue and tighter cost controls. Despite this, Affirm’s stock price fell about 10% following the earnings release. report. I think this decline is due to Shopify’s (store) gentle guidance Consider that Affirm is integrated into Shopify’s store POS. However, we believe that Affirm’s stock price decline could be an opportunity considering its growth potential due to increased BNPL spending, the possibility of interest rate cuts, and entry into overseas markets such as the UK. Based on this, I rate Affirm a Buy with a $105 price target by 2030, which implies a 225% upside from current levels.

3rd quarter overview

Affirm reported GMV of $6.3 billion in the third quarter of fiscal 2024, up 35.7% year-over-year. However, due to seasonal factors, sales decreased by 16% compared to the previous quarter, exceeding guidance of $5.8 billion to $6 billion. As a result, Affirm’s revenue increased 51% from $381 million to $576.1 million compared to the same period last year, but decreased 3% from $591 million compared to the previous quarter due to seasonality in Affirm’s business.

During the quarter, Affirm’s active consumers grew to 18.1 million, up 13.1% in You and 2.8% in QoQ, driven by increased adoption of the Affirm card, which surpassed 1 million cardholders shortly after the end of the quarter. At the same time, transactions per active consumer increased to 4.6 from 3.6 a year ago and 4.4 a quarter ago. Overall, there were 21.5 million transactions in the third quarter, 93.5% of which were returning customers. This is an increase of 49.3% compared to the same period last year and 17.9% compared to the previous quarter.

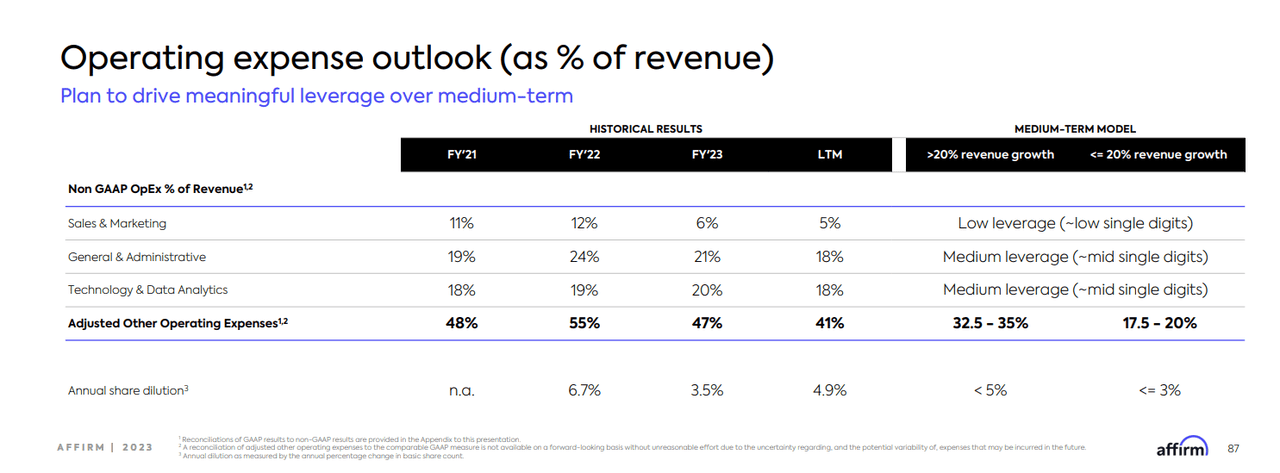

Looking at Affirm’s fixed costs, the company is showing tighter cost management compared to previous years. In the nine months ended March 31, Affirm’s technology and data analytics costs decreased year-over-year from $463.5 million to $377.6 million, making these costs account for 23% of Affirm’s revenue, compared to 41% a year ago.

The same could be said for sales and marketing expenses, which decreased from $493.1 million, or 43% of revenue, to $441 million, or 27% of revenue, over the same period. General and administrative expenses (G&A) expenses also decreased to $401.8 million, or 24% of sales, during the same period, compared to $458.8 million, or 40% of sales, the previous year.

These cost savings are a step in the right direction as they demonstrate that Affirm is on track to achieve its mid-term adjusted operating cost projections. In its recent investor day presentation, the company shared sales and marketing goals that represent low single-digit percentages of revenue, with technology and general and administrative expenses in the mid-single digits as a percentage of revenues.

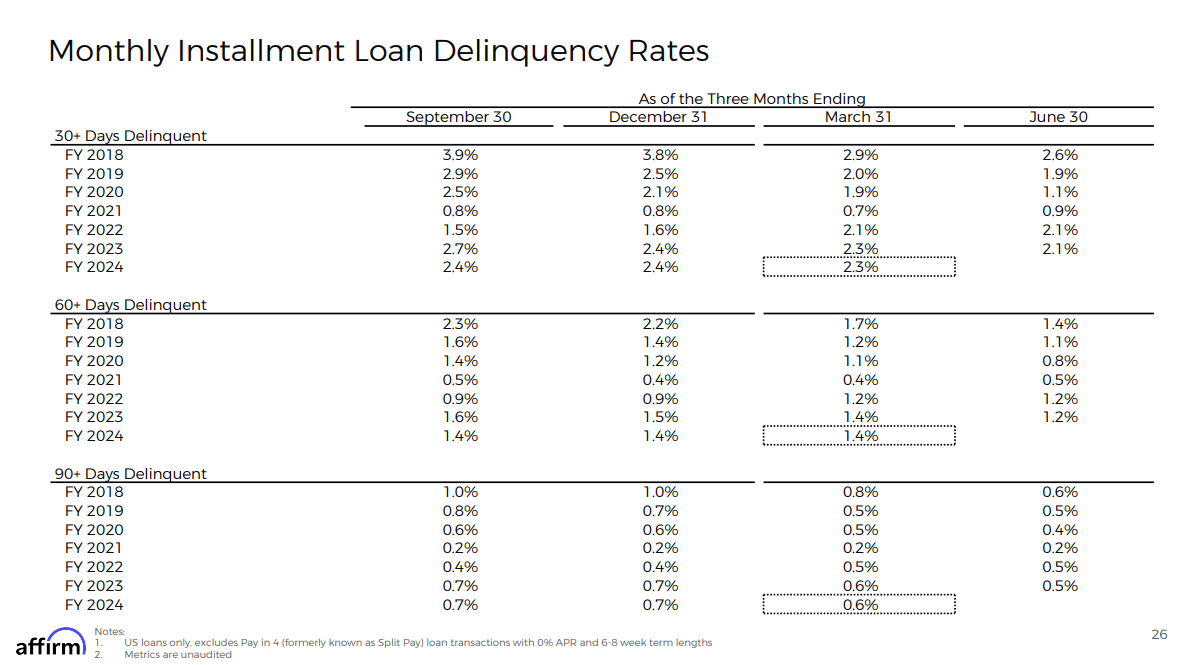

While the delinquency rate remained similar to the same period last year, the 30-day and 90-day cohorts showed a slight improvement compared to the previous quarter.

Fiscal 2024 Third Quarter Earnings Supplement

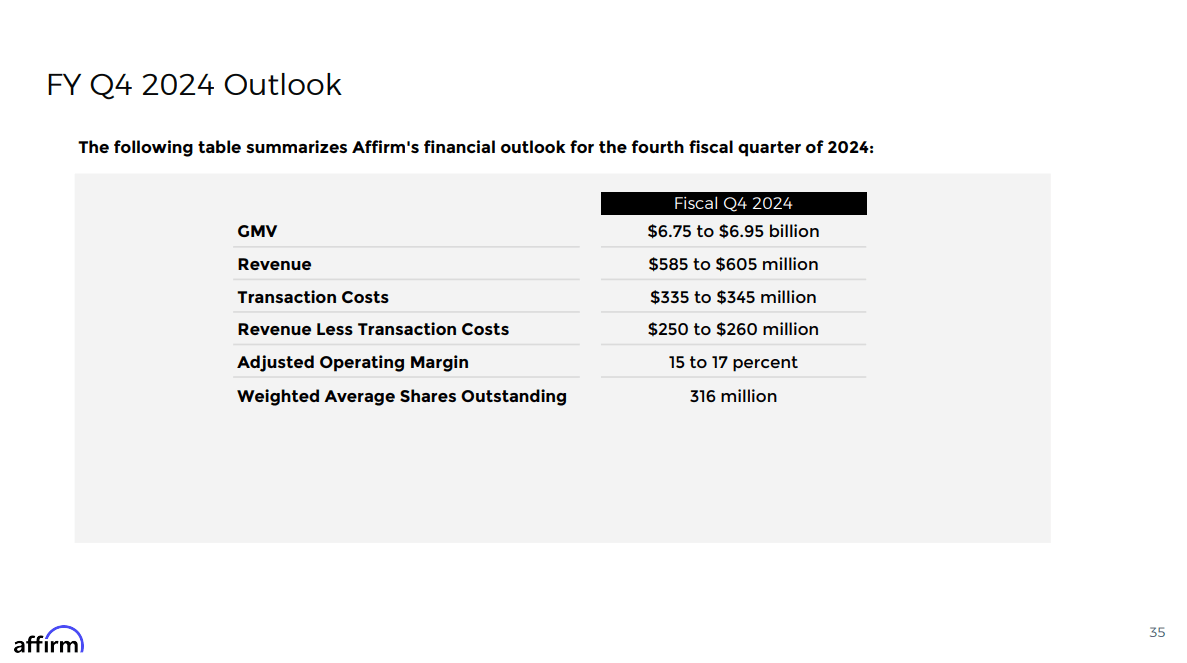

For the fourth quarter of fiscal 2024, Affirm is driving GMV between $6.75 billion and $6.95 billion, which would translate to full-year GMV between $26.1 billion and $26.3 billion and revenue between $585 million and $605 million. This implies annual revenue of between $2.25 billion and $2.27 billion, compared to analyst estimates. 2.26 billion dollars. At the midpoint of the company’s guidance, full-year revenue is on track to grow 42% YoY, in line with management’s forecast of 20%+ revenue growth over the medium term shared in its Investor Day presentation.

Fiscal 2024 Third Quarter Earnings Supplement

BNPL market growth

In my opinion, the main driver of Affirm’s future growth will be the growing adoption of BNPL payment methods. In a previous article covering Pagaya (PGY), I shared that 82.1 million U.S. consumers used BNPL for their spending and lending needs by the end of 2023, and that number is expected to reach 112.7 million by 2027. During this period, BNPL’s revenue is expected to grow from $71.9 billion to $124.8 billion by 2027, at a CAGR of 14.8%.

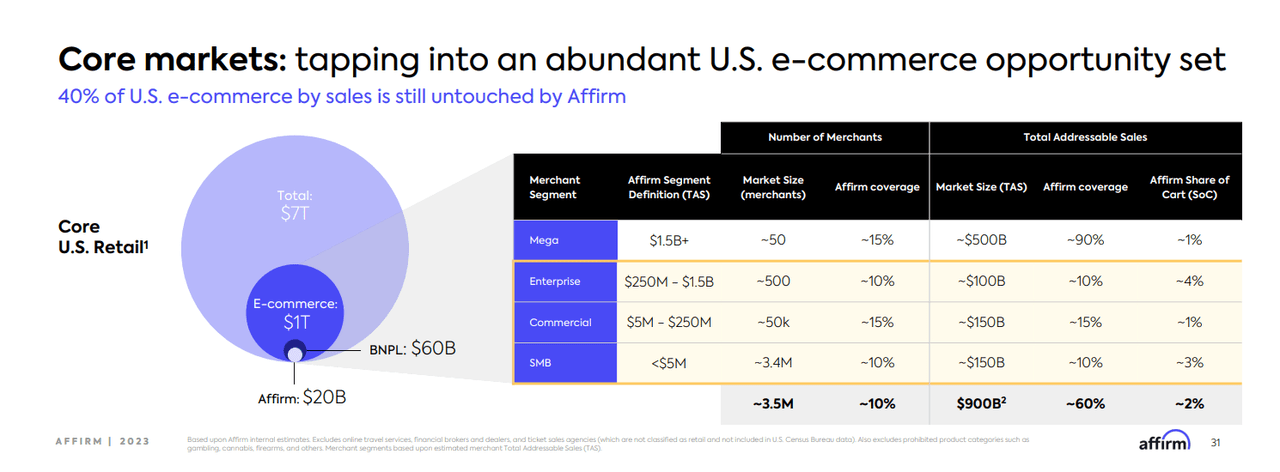

The expected growth in BNPL spending bodes well for Affirm’s growth potential, as it currently accounts for about 10% of U.S. e-commerce sellers. At the same time, coverage of total addressable e-commerce sales is approximately 60%. Accordingly, the expected increase in U.S. BNPL spending will be reflected in Affirm’s future GMV and, consequently, revenue.

Affirm’s Investor Day Presentation

Another tailwind for Affirm’s growth potential is the potential for interest rate cuts this year. Currently, Affirm offers payments on up to four purchases with interest rates between 0% and 36% depending on the consumer’s credit score. That means consumers with lower credit scores are more likely to receive interest rates closer to the 36% cap.

Because Affirm is not a bank, it offers BNPL loans to POS consumers through its funding partners. These partners are Cross River Bank, Celtic Bank and Lead Bank. That is, when interest rates fall, banks’ risk appetite generally increases as they relax their lending standards. Affirm may therefore be in a position to provide loans to more consumers who would otherwise be denied BNPL loans under current lending criteria. At the same time, Affirm can offer lower interest rates to consumers with lower credit scores, increasing transactions and ultimately increasing profits.

With this in mind, a rate cut could be coming after the April CPI figures showed inflationary pressures easing after three consecutive months of higher-than-expected CPI figures. In April, core CPI, excluding food and energy prices, rose 3.6% compared to the same period last year. This was in line with expectations and cooled from the 3.8% increase in March. Monthly core price increases of 0.3% were in line with expectations and down from 0.4% in the previous three months.

Thanks to April’s encouraging CPI print, investors are expecting two 25 basis point cuts in September and December this year, which would bring interest rates in the range of 4.75% to 5%, compared to the current range of 5.25% to 5.5%. It is expected. In addition to increasing loan sizes, lower interest rates will benefit Affirm by reducing its funding costs.

In the third quarter of fiscal 2024, Affirm’s funding costs increased 77% year-over-year due to higher benchmark interest rates on loans Affirm receives to fund BNPL loans and higher coupon payments on securitized loans. Therefore, a low interest rate environment could be a significant headwind to Affirm’s profitability outlook.

international expansion

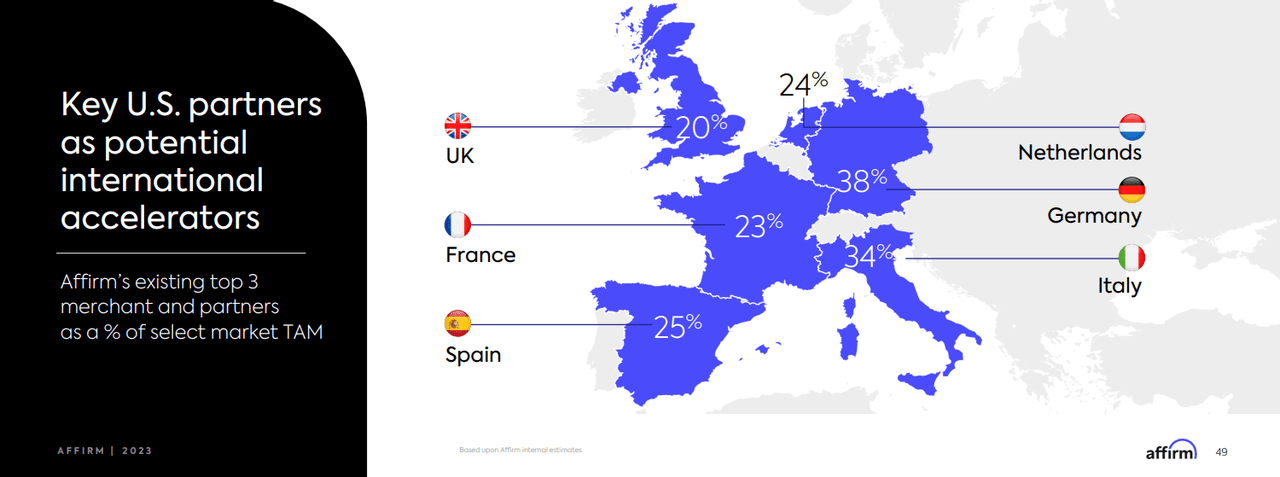

Another tailwind for Affirm’s future growth is its planned global expansion. The company’s main markets are the United States and Canada, but 60% of global e-commerce, excluding China, is outside of North America, leaving a large untapped global market. The next market Affirm plans to enter is the UK. The total market size in the UK is $133 billion and Affirm’s existing top three partners already have a 20% penetration rate in the UK market. This means that Affirm’s presence in the UK would give it access to a $26.6 billion market without even considering the possibility of securing more partnerships with sellers in the UK.

There are also opportunities in Europe’s best markets, as Affirm’s existing top three partners have penetration rates of 25% in Spain, 23% in France, 24% in the Netherlands, 34% in Italy, and 38% in Germany.

Affirm’s Investor Day Presentation

In my opinion, Affirm’s expansion into these markets as well as the UK will allow it to grow its GMV beyond its medium-term goal of $50 billion. Therefore, I am confident that Affirm can continue to grow its revenue by 20% or more in the near future.

evaluation

Given the expected growth of the BNPL market, the possibility of interest rate cuts, and Affirm’s growth potential as it expands globally, we believe it may be undervalued at its current valuation. We use the P/S ratio to value Affirm. That’s because the company is still unprofitable on a GAAP or non-GAAP basis and has yet to post positive adjusted operating income on a full-year basis. Therefore, I believe the P/S ratio is the best metric to value Affirm at this stage, given that my bullish argument for the stock is its earnings growth potential over the next few years.

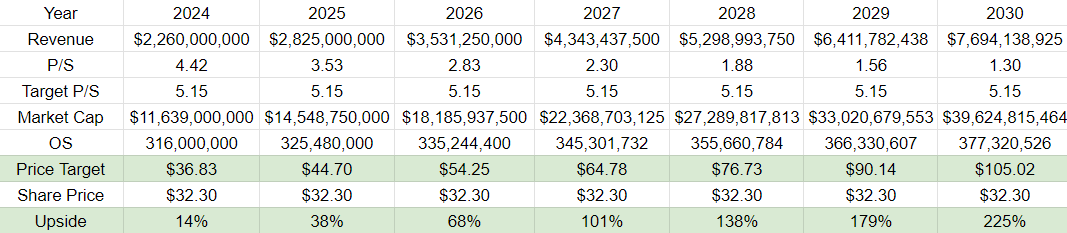

Affirm is driving 42% revenue growth at the midpoint of its guidance for this fiscal year, so it expects revenue to grow 25% in 2025 and 2026. Meanwhile, we expect revenue growth to slow from FY 2027 to FY 2030. That’s because Affirm is potentially maturing in new markets. Based on this, Affirm’s sales forecast until fiscal 2030 is as follows.

|

year |

revenue |

growth |

|

2024 |

$2,260,000,000 |

|

|

2025 |

$2,825,000,000 |

25% |

|

2026 |

$3,531,250,000 |

25% |

|

2027 |

$4,343,437,500 |

23% |

|

2028 |

$5,298,993,750 |

22% |

|

2029 |

$6,411,782,438 |

21% |

|

2030 |

$7,694,138,925 |

20% |

My prediction is that Affirm will trade at the following P/S ratio:

|

year |

revenue |

P.s |

|

2024 |

$2,260,000,000 |

4.42 |

|

2025 |

$2,825,000,000 |

3.53 |

|

2026 |

$3,531,250,000 |

2.83 |

|

2027 |

$4,343,437,500 |

2.30 |

|

2028 |

$5,298,993,750 |

1.88 |

|

2029 |

$6,411,782,438 |

1.56 |

|

2030 |

$7,694,138,925 |

1.30 |

Meanwhile, my projections are that dilution will be less than 3% per year, as shared in a recent Investor Day presentation.

Affirm’s Investor Day Presentation

Given that Affirm has shared that it expects its outstanding shares to reach 316 million at the end of FY 2024, and assuming 3% dilution thereafter, Affirm’s outstanding shares by FY 2030 are expected to be: It’s possible.

|

year |

OS |

dilution |

|

2024 |

316,000,000 |

|

|

2025 |

325,480,000 |

three% |

|

2026 |

335,244,400 |

three% |

|

2027 |

345,301,732 |

three% |

|

2028 |

355,660,784 |

three% |

|

2029 |

366,330,607 |

three% |

|

2030 |

377,320,526 |

three% |

Although Affirm is the only BNPL listed company, we believe its valuation is comparable to other growth-stage fintechs such as Upstart (UPST) and Marqeta (MQ). However, Upstart and Marqeta are trading at forward P/S ratios of 4.66 and 5.64, respectively. That means the average P/S ratio between the two companies is 5.15. Using this multiple, Affirm’s target price through fiscal 2030 is:

own calculations

danger

Risks to my bullish thesis include Klarna’s potential IPO in the first quarter of 2025, as reported by Sky News. Klarna has secured support from shareholders and regulators to set up a UK-registered holding company in preparation for a New York IPO, according to reports. Because Affirm is currently the only pure-play BNPL investment on the market, Klarna’s potential IPO could provide investors with an opportunity to diversify their exposure to the BNPL market, which could reflect negatively on Affirm’s valuation.

Another risk to consider is competition. The BNPL industry has low barriers to entry and is highly competitive, allowing many startups to enter the market. At the same time, several large banks are jumping into this space, including card issuers like American Express (AXP), as well as big banks like US Bancorp (USB), Citigroup (C), and JPMorgan Chase (JPM). These institutions have an advantage over BNPL providers because they have extensive credit card networks and can serve merchants at lower prices than BNPL providers like Affirm.

conclusion

With the stock down 10% since strong Q3 FY 2024 results, we believe the current decline is an attractive entry point for Affirm. BNPL providers continue to record impressive GMV and revenue growth despite the current high interest rate environment and are demonstrating tighter cost management.

With this in mind, Affirm expects to continue to see strong revenue growth in the near future due to increased adoption of BNPL payments and potential interest rate cuts starting this year. Meanwhile, Affirm’s international expansion in the UK and potential expansion into Europe could drive further GMV growth as existing partners already have high penetration in this market. Taking this into account, I rate Affirm a Buy with a $105 price target by 2030, which implies a 225% upside from current levels.