Figs: The recent rebound was not justified by fundamentals and the stock remains on hold (NYSE:FIGS)

")

Catherine Delahaye/DigitalVision via Getty Images

FIG (New York Stock Exchange: Fig) is a healthcare clothing retailer known for its high-quality, trendy scrubs.

I started covering the company with a Hold rating in March 2024. The rating was based on the company’s low operating margins and dilutiveness. Stock-based compensation, slowing growth trends, and increased competition. The company’s adjusted EV was too high compared to its operating profit margin.

In this article, we will review the company’s 1Q24 performance and earnings release. Results were not what was expected, with revenues flat and margins declining thanks to an investment program the company launched last year. However, the stock received a very positive response, rising 20% within a few days of the earnings release. Given that this rise in the stock price is unjustified relative to the company’s fundamentals, we believe the stock has much less opportunity today than it did in March.

unimpressive results

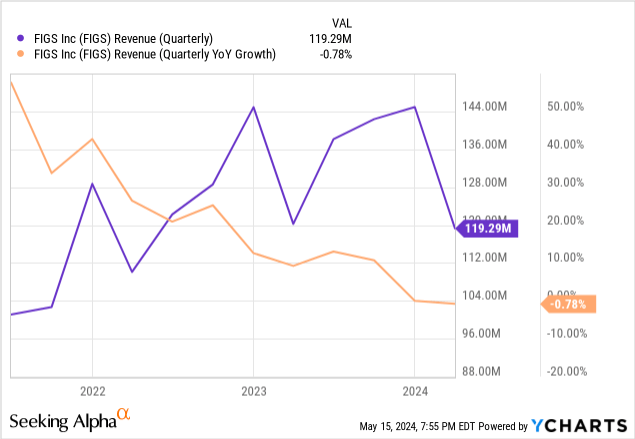

uniform return:FIGS recorded a low- or no-growth quarter in the second quarter, with sales down 0.8%. According to 1Q24 MD&A, the company saw a 9% increase in customers, but this was offset by lower purchase frequency given the flat AOV.

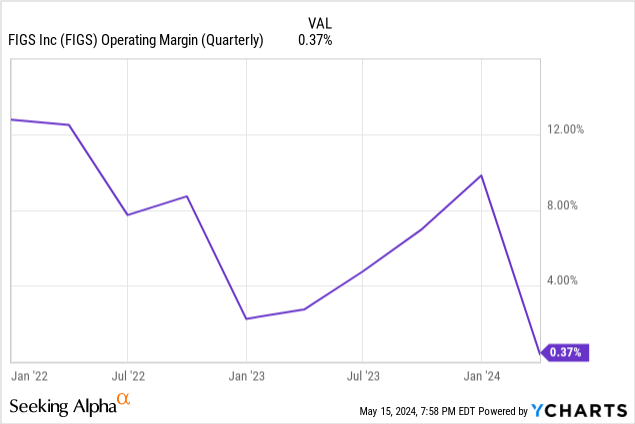

Investment eats up margins: FIGS’ operating profit margin was low enough to be close to the break-even point for the quarter. Margins would be expected to be lower given that the first quarter was the smallest quarter due to seasonality, but in this case the decline was even greater due to increased investment.

Changes in product and geographic mix decreased FIGS’ gross margin. The company is selling more non-scrub products internationally and is banking on the newest addition to its scrub line. The international segment accounts for less than 10% of revenue and the non-scrubbing segment accounts for about 20% of revenue, but these categories have lower margins because the company does not operate at the same scale as its core markets. Figs expects margins to improve with scale in the medium term.

Cost of sales decreased due to accounting changes for export tariff treatment, but is expected to increase in the coming quarters as the company moves through its fulfillment center transition.

Lastly, although marketing was sluggish, management noted its commitment to maintaining investment in brand marketing. The company launched the campaign with documented wildlife veterinarians in South Africa. Recently, we launched another campaign around Nurses Week, bringing nurses from across the country to ring the bell at the NYSE.

Therefore, most of the cost increases came from growth investments, such as new products and changes to the company’s fulfillment centers, rather than reductions in marketing.

However, G&A grew by 5% compared to the same period last year. I generally dislike this category of expenses because this is where most of a company’s cost overruns lie. For example, G&A includes executive compensation (two of FIGS executives earned $10 million in FY23) and headquarters expenses.

Management’s ‘strong’ cash flow: Company executives talked several times during the call about strong, solid cash flow generation. However, management was completely insincere about this. In fact, the company generated $12 million in FCF in 1Q24, but $11.6 million was in stock-based compensation. This is not a strong cash flow generation model. That’s simply paying the costs in stock and diluting shareholders. This means that sincerity, which is the basis of trust between shareholders and management, is lacking. In my opinion, it’s very bad.

Valuation reconsidered after rally

Some market participants may have been more satisfied with the company’s performance. That’s because Figs’ stock price soared 20% after the earnings release. Perhaps some investors see stagnant earnings as a sign of a bottom and are speculating that the company will return to growth.

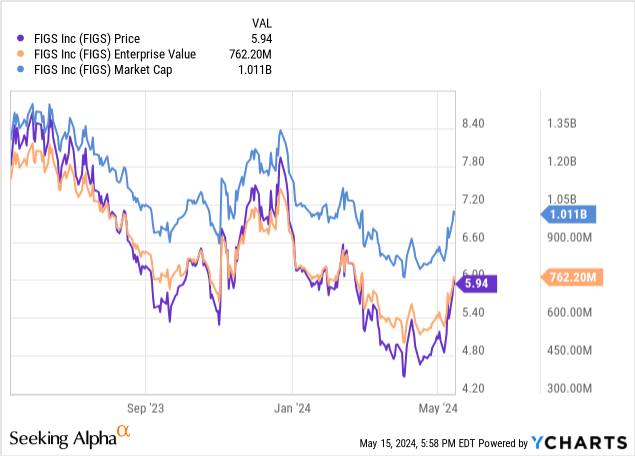

The chart below shows Figs’ EV is $760 million, but I think the company needs to adjust the stocks and options it uses to generate the ‘strong cash flow’ mentioned above. The figure below is based on 170 million shares, but up to 35 million additional shares can be issued in the form of RSUs and options. Combined, this gives the company a market capitalization of $1.22 billion and an EV of $970 million.

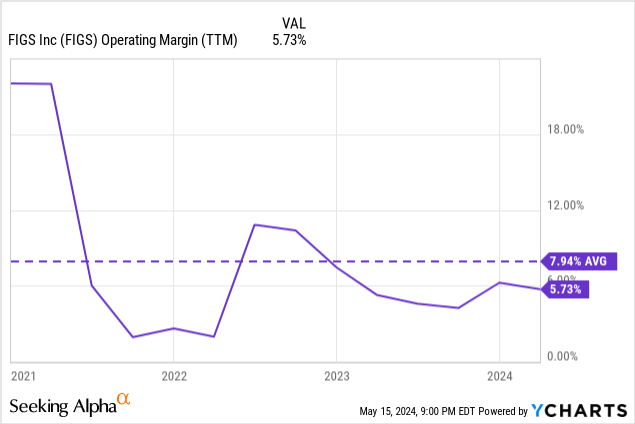

What expectations lie behind these assessments? For example, for a company to generate a 15x EV/NOPAT multiple ($65 million in NOPAT or $92 million in operating income), the company’s operating margin would need to be 17% (and 12%), about 10 percentage points above the company’s historical average. It must be. points above your current level).

Conversely, to achieve the same EV/NOPAT multiple while still earning an 8% operating margin, FIGS would need to increase revenue by 110% from current levels, to $1.15 billion.

Therefore, in order to provide a reasonable (in my opinion still high and certainly not opportunistic) multiple on earnings, the current stock price must imply extremely optimistic assumptions, such as duplication of revenue or duplication of historical margins. Even if these amazing achievements are realized, the stock will still be reasonably valued.

Therefore, I don’t think Figure’s stock price is an opportunity at this price.

What to Look for in Future Returns

I think two topics are essential for future Figs.

The first is international sales, and given the product’s success in the U.S., we believe this is one of the key opportunities for the company. I would guess that Figs’ customer awareness in the US is already very high among doctors, nurses, dentists, etc. This leads us to believe that the company has probably already captured most of the market opportunity in the United States. People who aren’t buying Figs today probably have a reason to do so (such as high prices) rather than simply not knowing about the company. However, many professionals in Europe, Canada, Asia and Australia have never used Figs’ excellent products and may become customers.

The second is competition in the United States. My coverage launch article mentioned several DTC brands operating in the high-quality scrub space. Given their extremely high gross margins of over 60%, these companies have a lot of room to drive Figs down on price. Signs of increased competition include increased promotional activity for FIGS in the U.S. or significant hits to gross margins that are not accounted for by changes in product mix.