The Ethereum Foundation is still selling ETH after staking 70,000 coins.

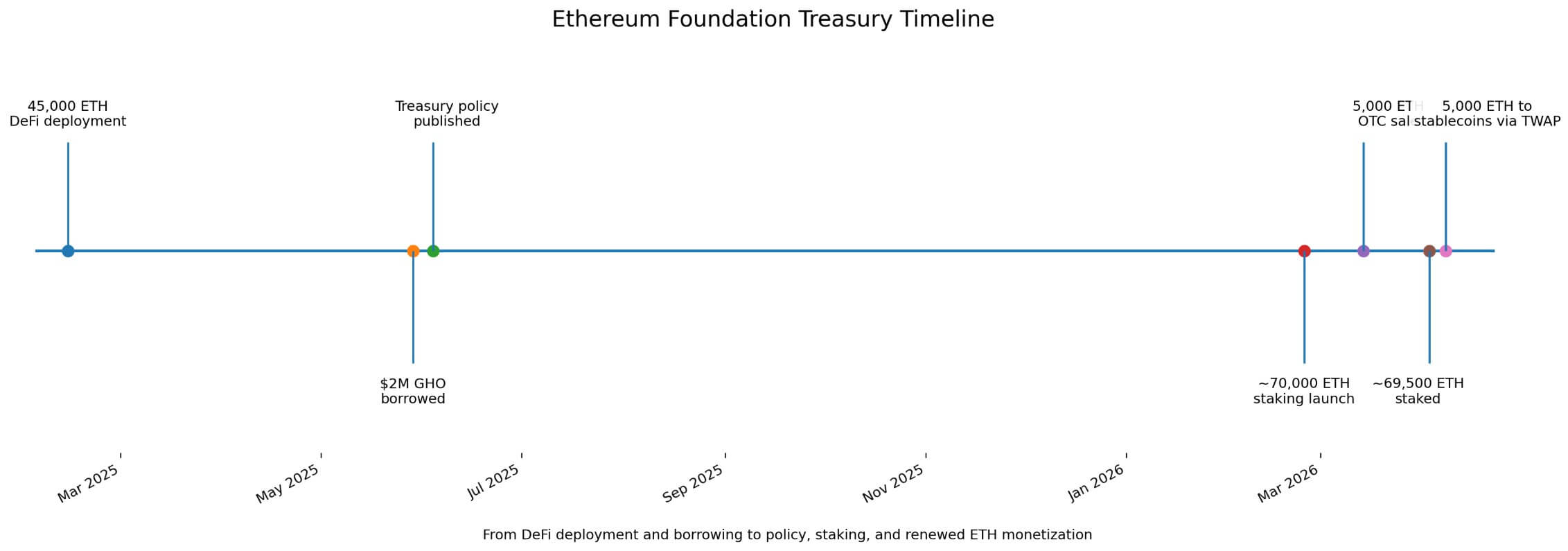

The Ethereum Foundation (EF) announced on April 8 that it will convert 5,000 ETH to stablecoins through CoWSwap’s TWAP feature to fund research, grants, and donations.

The announcement has reignited debate about what the foundation’s financial overhaul will achieve. Last year, EF moved treasury assets into DeFi and launched a staking initiative centered on about 70,000 ETH after borrowing against ETH collateral.

The realities outlined in EF’s June 2025 Financial Policy suggested a different model. This tied monetization to fiat-denominated operational buffers and kept ETH sales, staking, and stablecoin borrowing within the same financial framework.

On February 13, 2025, EF Treasury announced that it had distributed 45,000 ETH to Spark, Aave Prime, Aave Core, and Complex. On May 29, it borrowed $2 million from GHO against its Aave position.

This move has symbolic significance as it demonstrates that EF will not sell physical ETH, but will use DeFi rails to raise working capital.

In early April, this interpretation filtered into retail discourse, with a Reddit post claiming that EF was “no longer selling it.” One netizen responded, “I’m glad they stopped selling it.”

Despite anecdotal evidence, this kind of conversation suggests that a stronger version of the paper was already in circulation before EF announced the switch on April 8.

Sales continue

EF launched its staking plan on February 24th, stating that 70,000 ETH would be staked and the rewards would go to the Treasury.

On March 14, we completed a 5,000 ETH OTC sale on BitMine at an average price of $2,042.96. On April 3, the total staked amount due to on-chain activity was close to the target, at approximately 69,500 ETH. Then came the CoWSwap switch on April 8th, highlighting that selling and staking had already been running side by side for several weeks.

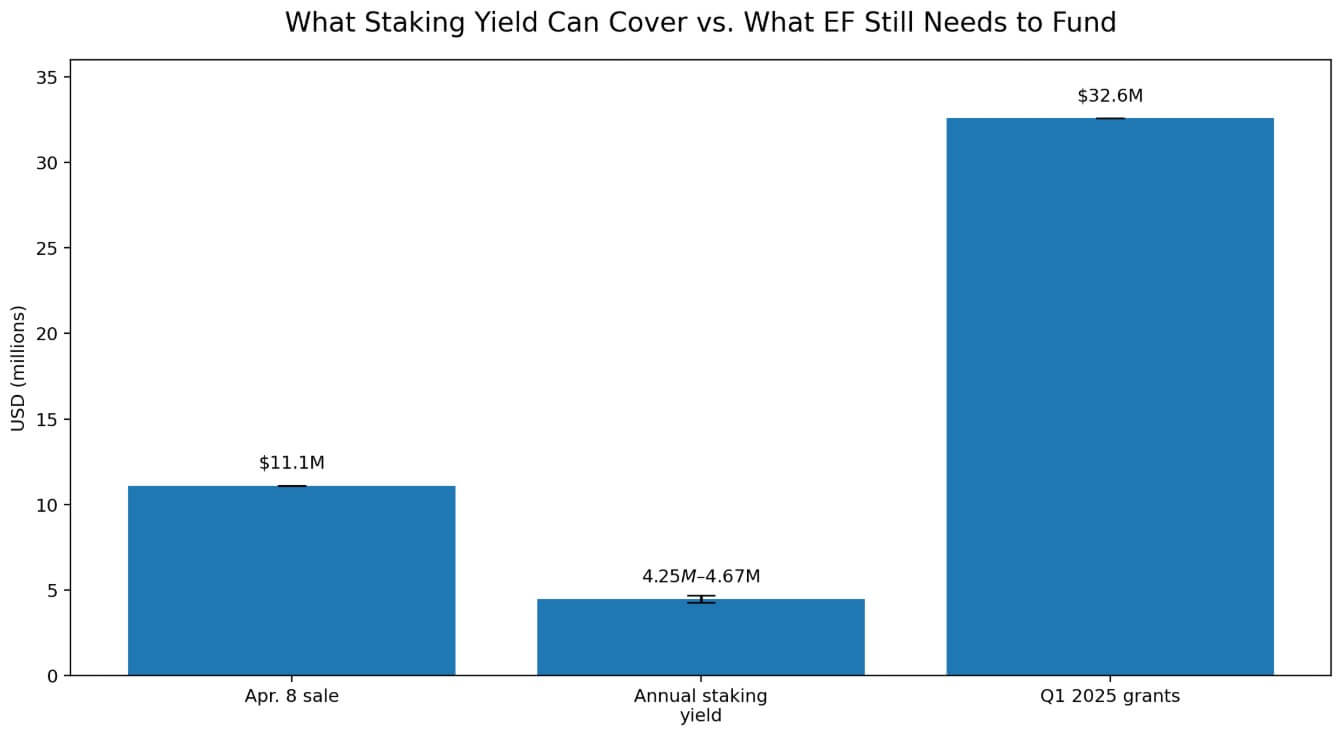

If the ETH price is around $2,220.76, converting 5,000 ETH is equivalent to about $11.1 million, and the benchmark ETH staking interest rate in early April was about 2.73% to 3.00%.

Applied to 70,000 ETH, it would produce approximately 1,912 to 2,102 ETH per year, worth approximately $4.25 to $4.67 million at current prices. A single 5,000 ETH sale equates to approximately 2.4-2.6x the annualized return of a full 70,000 ETH staking sleeve.

Staking programs improve treasury efficiency and reduce funding requirements, but are still well below the scale needed to replace treasury sales.

The EF June 2025 framework sets annual operating costs at 15% of the treasury and an operating buffer at 2.5 years. This means that fiat-denominated reserves are equivalent to 37.5% of the Treasury.

EF’s last full financial snapshot, the October 31, 2024 report, taken only as an example, shows total finances at $970.2 million and non-crypto assets at $181.5 million, implying policy target reserves of approximately $363.8 million.

EF has already added to its stablecoin exposure publicly since that snapshot, deploying 2,400 ETH and approximately $6 million in stablecoins to Morpho in October 2025, and later announced additional ETH to stablecoin conversions in October 2025 and April 2026.

The exact current size of EF’s fiat bucket and whether tokenized RWA holdings have already added to the material size are not yet known. Therefore, the 2024 snapshot should still be treated as an example rather than a replacement for today’s balance sheet.

According to EF’s own allocation update, grants for the first quarter of 2025 were $32.6 million. At current ETH prices, this is equivalent to approximately 14,700 ETH. The April 8 transition covers only about 33% of the total grant funding for the quarter, excluding protocol research, staffing, operations and broad industry support.

Yields and borrowings remain within fiat-denominated budgets and periodic revenue generation is still required.

potential consequences

The bullish case for EF is based on simple Treasury arithmetic, as higher ETH prices and lower long-term operating expense ratios allow the foundation to monetize fewer coins while maintaining a dollar buffer.

| script | What changes | Potential financial impact |

|---|---|---|

| bull incident | ETH price rises, long-term OpEx ratio falls | Fewer coins need to be sold to maintain fiat buffer. |

| base case | Mixed strategies continue | Staking, DeFi, lending, and regular sales coexist. |

| bear case | ETH price weakens, spending pressure increases | We may need to cash out more ETH to preserve runway. |

| main meaning | Reserve targets are maintained in fiat denominations. | If ETH falls, the “less sold” narrative falls apart |

In this environment, staking rewards and selective borrowing could reduce quarterly revenue and provide EFs with more flexibility in venue selection through OTC blocks, TWAP execution, or conservative DeFi positions.

Treasury modernization will then emerge at a lower pace, at a smaller clip, and with better execution.

Since EF’s reserve targets are denominated in fiat, the bearish case follows the same framework in reverse.

A weakening ETH price could force more monetization to preserve runway. This is especially true if the foundation relies on a countercyclical mission and spends more aggressively in difficult market conditions.

In that setup, large staking sleeves will still generate returns, but reserve requirements can increase faster than the returns offset them.

Public expectations built around “lower sales” conflict with the balance sheet discipline EF has already enshrined in its policy.

The conversion of April 8 brought the discipline back into view. EF’s financial strategy already included a combination of DeFi deployment, stablecoin borrowing, staking, and regular ETH sales.

The market narrative extended beyond the written policies and the foundation’s own post-staking trading records.