Credo Brand Marketing IPO Review

Credo Brand Marketing IPO Review: Credo Brand Marketing Limited is an Indian Western casual wear manufacturer. The company plans an IPO that will open on December 19 and close on December 21, 2023. The 550 Cr issue will be listed on December 27, 2023.

Let’s find out a little more about the company and its market presence. We’ll then take an overview of the industry and see if the company has room to expand. Finally, just before concluding, let’s examine the company’s financials and find out its strengths and weaknesses.

Credo Brand Marketing IPO Review – About Us

Credo Brands Marketing is the brand’s parent company. mufti, A brand that redefines menswear in the casual category. The brand had humble beginnings in 1992 when promoter Kamal Khushlani was paid Rs. 10,000 loan to set up his fashion retail brand.

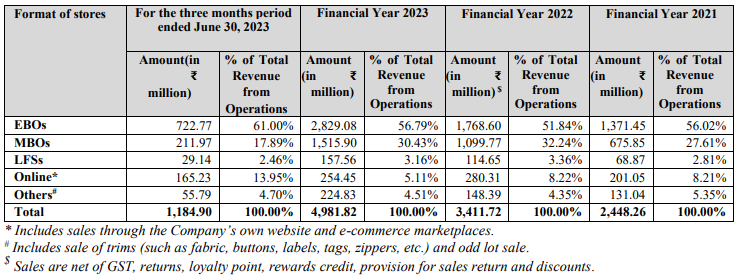

From a single store in Mumbai, the brand has a presence in over 591 cities. The company currently has a pan-India distribution network. Exclusive Brand Outlet (EBO), Large format stores (LFS)and Multi-Brand Store (MBO)With online activities.

The brand offers a variety of men’s western clothing, including sweatshirts, jeans, cargo, chinos, jackets, blazers, and sweaters. It is a brand that designs a variety of clothing, including comfortable holiday casual, authentic daily casual, urban casual, party wear, and athleisure.

The company earns most of its revenue from its exclusive brand outlets, which contribute between 52% and 61% of its revenue. Multi-brand outlets bring in up to 27% to 30% of sales, but MBOs have reduced sales to 17.89% in Q1 2023. Mufti’s presence in large stores earned the lowest return at 3.16% in FY23.

Credo Brand Marketing IPO Review – Industry Insights

The retail market value in India was Rs. 36 Lakh Cr (USD 461 Bn) in FY15 and its value has reached Rs. 76 Lakh Cr (USD 951 Bn) in FY23. The market size is expected to grow at an average annual rate of 10.4%, reaching 1.3 trillion won. 113 Lakh Cr (USD 1418 billion) by 2027.

This retail market includes everything from clothing and accessories to home appliances, watches and jewelry. The clothing and accessories market share of the overall retail market is only 7% and is expected to increase to 9.5% by 2027.

The men’s apparel market was estimated at 2.2 Lakh Cr in FY23, growing at a CAGR of 9.6% from FY15-20. The market expects it to achieve a strong growth rate of 18% CAGR, reaching Rs. 4.3 Cr by FY27.

According to a Technopark report, the market share of organized players in the men’s clothing category stood at around 45% in FY22. This share is expected to increase to around 60% by FY27. The men’s western market accounts for approximately 94% of the total men’s clothing, with the remainder belonging to the western apparel market.

Like companies introducing the Casual Fridays concept, India’s youth and the casualization of menswear fashion are expected to drive the menswear market in the future. The growing demand for fusion clothing, a mix of Western and Indian styles, is likely to be a trendsetter in the next decade.

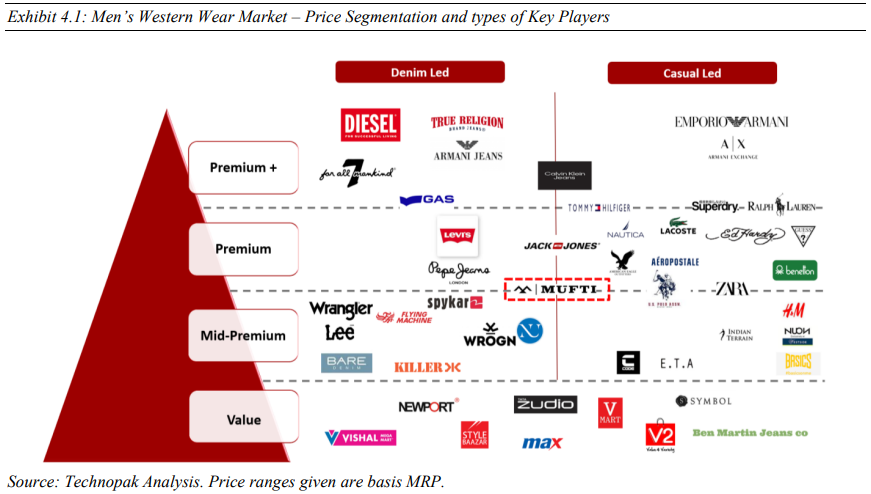

Brand Mufti stands at the pinnacle of the premium and mid-premium segment. Let’s take a look at how Mufti compares to its peers.

Credo Brand Marketing IPO Review – Financials

Credo Brand reported revenue of Rs. 509 Cr in FY23, up 43% from Rs. 355 Cr in FY22. Since FY21, the company has grown its revenue at a CAGR of 40%.

During the same period, net profit increased by 117% to 10 billion won. 36 Cr in FY22 to Rs. 78 Cr in FY23. Net profit has grown at a CAGR of 375% since FY21.

The company maintained industry-leading EBITDA and PAT margins of 32.89% and 15.56%, respectively. The significant increase in net profit was driven by margin expansion from 1.41% in FY21 to 15.56% in FY23.

Credo Brand Marketing – Key Players

Compared to listed companies, Credo is the smallest company by revenue. The company holds just 4% of retail giant Aditya Birla Fashion Ltd.

Credo’s closest competitor is Go Fashion (India), a leading manufacturer of women’s leggings sold under the brand name Go Colors. Credo’s sales are about 75% of Go Fashions.

Go Fashions is currently trading at a PER of 88.24x on the exchange, while Credo is trading at a PER of just 23x. Another thing to note is that Credo Brands currently has a much better ROE and ROCE compared to Go Fashion (India).

Company Strengths

- The company outsources entire production to produce on a large scale. This eliminates high labor costs. The brand’s stores sign leases for five to nine years, allowing the company to maintain an asset-light model.

- Credo has a professional design team with rich experience working in global and domestic retail markets. This exclusive team of 17 people has selected over 682 designs as of the first half of 2024.

- The company has 404 EBOs across the country, of which 66% are located on high streets, 32% in shopping malls and 1.5% in airports. These stores bring in most of the company’s revenue.

- The company enjoys industry-leading EBITDA and PAT margins of 30% and 15%.

- After FY21, Credo succeeded in increasing ROE and ROCE from 5.86% and 1.81%, respectively, to 28.16% and 29.98% in FY23. This shows signs of effective financial management.

company’s weaknesses

- The company operates in a highly competitive market with a variety of international brands. Keeping up with market trends and capturing market share will be the company’s biggest challenges.

- The brand focuses specifically on men’s casual clothing. A drastic change in male consumer preferences can have a major impact on brands. Therefore, diversification is necessary.

- The company derives its entire revenue from selling products under just one brand. mufti. Again, some diversification will reduce your brand’s exposure to just one segment.

- Like any organized retail business, the company runs the risk of holding unsold inventory. Current inventory turnover days increased from 154 days in FY23 to 198 days in Q1FY24.

Credo Brand Marketing IPO Review – GMP

GMP is currently not available. We will update the article as we receive information.

Key IPO Information

promoter: Kamal Khushlani

Book Operations Lead Manager: DAM Capital Advisors Ltd, ICICI Securities Ltd and Keynote Financial Services Ltd

Proposal registered by: Link Intime India Pvt Ltd

purpose of the problem

- To provide a profitable exit to the promoters of the company.

- To enjoy the benefits of listing on the exchange.

conclusion

This concludes the Credo Brands IPO. A company issues shares only when it succeeds in expanding market power and maximizing profits. Additionally, the issue price is Rs. 280, the company’s P/E is 23x, which seems reasonable, especially considering the earnings growth rate.

Go Fashion (India), a peer of Credo, was listed two years ago on December 3, 2021. The IPO was listed at a bumper premium of 80%. However, after the IPO listing, new shareholders were disappointed and received only a small profit (~4%) after the listing. Despite this, Go Fashion registered as a loss maker and recorded a profit only in FY22.

So what will happen to Credo Brands in its IPO listing? Is the stock attractive enough to add to your portfolio? Let us know in the comments below.

Written by Nasir Hussein

by utilizing stock screener, stock heatmap, Backtesting Portfolioand stock comparison The tools on the Trade Brains portal give investors access to comprehensive tools to identify the best stocks, stock market newsBe aware and invest well.

Start your stock market journey now!

Want to learn stock market trading and investing? Check out exclusive stock market courses from FinGrad, a learning initiative from Trade Brains. You can sign up for free courses and webinars from FinGrad and start your trading career today. Sign up now!!

")