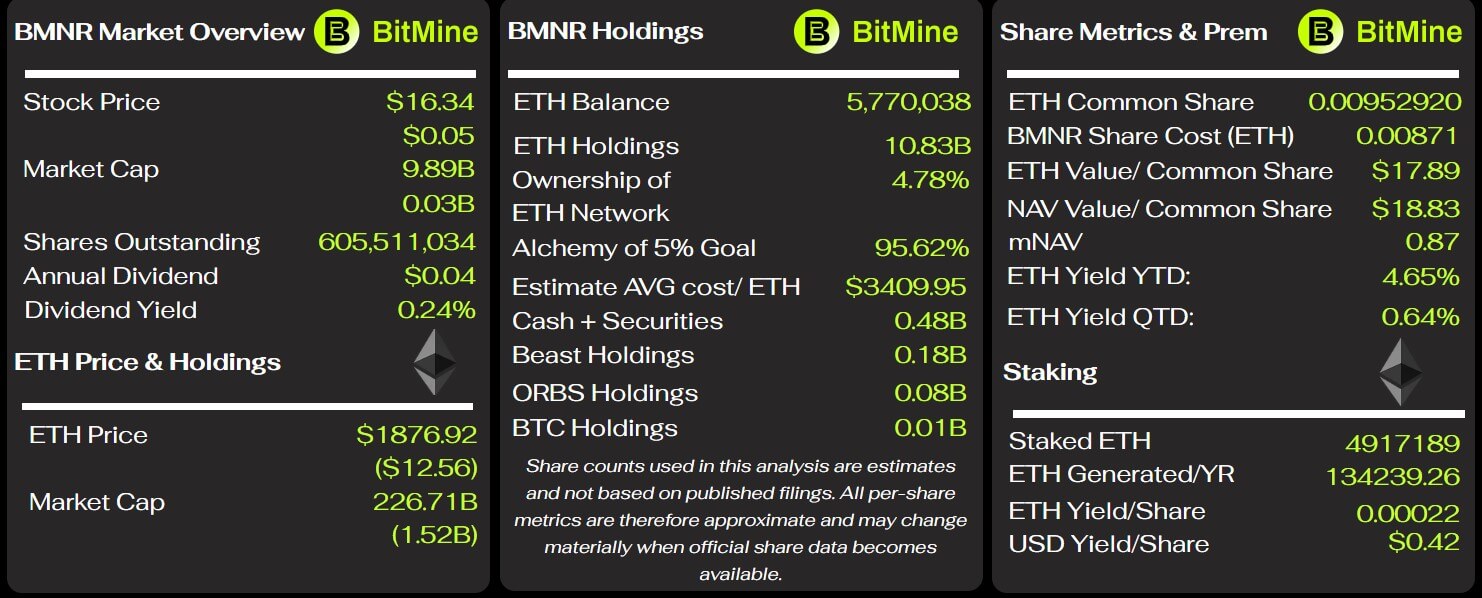

BitMine made $46 million from Ethereum staking but lost twice the amount it staked.

BitMine’s efforts to turn one of the world’s largest corporate Ethereum holdings into a recurring income stream generated about $46 million through staking last quarter.

But options losses of $92.1 million dwarfed those gains, and rising financing costs and an aggressive share issuance further weakened the economics for existing shareholders.

In its fiscal third quarter, which ended May 31, the company reported that revenue jumped to $46.5 million from $2.1 million in the same period a year earlier. Approximately 98%, or $45.7 million, came from staking and verification as BitMine accelerated its transition from Bitcoin mining to an Ethereum-centric financial model.

Despite this growth, the company posted a net loss of $83.6 million, compared to a loss of $623,000 during a similar quarter last year.

The option loss wipes out BitMine’s initial Ethereum staking profits.

The biggest immediate impact on BitMine’s quarterly results was the company’s options strategy.

BitMine recorded losses of $92.1 million on Ethereum-related derivatives during the quarter, roughly double the revenue it generated from staking operations over the same three months.

The company incurred a loss of $78.6 million due to the net impact of options contracts expiring during the period, with an additional $14 million due to exercised positions. The $534,000 gain on contracts that remained outstanding provided only a small offset.

BitMine had no derivatives activity for a similar quarter last year, which led to a drastic change in the risk profile of its treasury operations.

Derivatives losses totaled $133.3 million in the first nine months of the fiscal year. This included losses of $79.3 million from exercised contracts and $54.5 million from expired positions, partially offset by a gain of $515,000 from open contracts.

During the same period, BitMine generated $56.9 million through staking and verification. So the derivatives losses were more than double the income earned by staking ETH to help validate transactions on the Ethereum network.

BitMine said its strategy primarily consisted of selling put options as part of a broader financial management program.

While these contracts can generate premium income or facilitate the purchase of assets, they can also result in significant losses if market prices move against the seller or if the contracts are settled under unfavorable terms.

The scale of BitMine’s losses suggests that its attempts to generate additional revenue from options have offset the gains it has made so far from its verification infrastructure.

Meanwhile, the company’s general and administrative expenses also increased to $37.3 million from $744,000 a year ago. Management attributed the increase to digital asset custody and treasury management fees, increased salaries, and increased cash and stock-based compensation for directors.

Before the digital asset valuation change, staking revenue still covered the company’s quarterly selling and administrative expenses. Even excluding several non-cash items, BitMine’s own non-GAAP calculations showed an adjusted net loss of approximately $70.8 million.

This distinction is key to your filing. The verification business began generating meaningful recurring revenue, but the broader financial strategy depleted those profits.

BMNR stock sale converts financial growth into shareholder dilution

BitMine’s rapid accumulation of Ethereum was primarily funded through public stock markets, with most of the funding burden passed on to ordinary shareholders.

During the nine months ended May 31, the company sold approximately 340.7 million BMNR shares through the marketplace program, raising $11.87 billion after deducting issuance costs. During the same period, BitMine spent approximately $11.69 billion purchasing ETH.

The resulting dilution was significant. The number of common shares outstanding increased 149% in nine months, from 232.4 million shares at August 31, 2025 to 579.7 million shares at the end of May 2026. The share count continued to grow after the quarter, reaching 603.2 million shares on July 9.

As of May 31, this equity funding expansion has allowed BitMine to accumulate 5.42 million ETH at a cumulative cost of $19.05 billion. The company’s ETH holdings have expanded to 5.7 million ETH as of press time.

Meanwhile, total reserves as of May 31 were valued at $10.86 billion, about $8.2 billion (43%) below quarter-end expenses.

The decline accounted for most of the company’s unrealized digital asset losses of $9.04 billion in the first nine months of the fiscal year. BitMine posted a total net loss of $9.1 billion in the period.

The size of the cut highlights the exposed shareholders BitMine is assumed to have issued shares to acquire ETH at prices well above its book value on May 31.

Nonetheless, the company’s shareholders approved an increase in authorized common stock from 500 million shares to 50 billion in January.

While this approval does not require BitMine to issue the full amount, it provides management with significant capacity to continue to raise assets for digital asset purchases and other investments.

BitMine warned that its ability to expand its treasury depends in part on continued access to capital markets. A decline in ETH, a decline in BitMine’s stock price, or weakening investor demand could make additional financing more expensive or limit the Company’s ability to issue securities on favorable terms.

Therefore, the model relies on more than staking returns and final Ethereum valuation. Additionally, shareholders must remain willing to fund additional accumulation despite rapid dilution and a financial position with billions of dollars in unrealized losses.

Long-term contracts increase the cost of generating ETH yields.

As BitMine expands staking to offset financial volatility, the contracts supporting these operations add fixed and revenue-linked costs that narrow the economics of the strategy.

The company recorded quarterly expenses of $12.8 million under a 10-year consulting agreement with Ethereum Tower, a third-party service provider that provides consulting, asset management, custody and staking services.

This amount represents approximately 28% of the staking and verification revenue generated during the period.

Costs under this contract totaled $37.5 million in the first nine months of the fiscal year. BitMine expects annual costs to range from $40 million to $50 million, based on tiered fees calculated on the value of digital assets under management.

The contract cannot be canceled except in limited circumstances. If BitMine terminates it without cause, the company may be required to pay Ethereum Tower 85% of the fees it would have incurred for the remaining period.

BitMine also signed a separate 10-year managed services agreement with Ethereum Tower after acquiring Pier Two, the MAVAN validator operations division.

Under the agreement, Ethereum Tower will be entitled to receive 2% membership interest from MAVAN and monthly payouts calculated as a percentage of native staking rewards generated through the platform.

BitMine had not recorded any costs under the second contract as of May 31. Therefore, the revenue-linked costs of those contracts have not yet appeared in the staking margins reported by the company.

The company stated that a significant portion of its ETH holdings have been staked through MAVAN, and that it expects staking rewards to exceed asset management costs.

Recent quarters have provided early support for these expectations at the operational level. Staking profits before cryptocurrency valuation changes include selling and administration costs.

However, long-term consulting fees, future revenue share payments and extensive financial management costs mean that economics cannot be measured based on total staking returns alone.

Although there is no debt, BitMine’s dependence on capital markets deepens.

BitMine maintained some leverage, with $340.3 million in cash and $433.1 million in working capital as of the end of May, and no existing debt.

Total liabilities were approximately $30.1 million against reported assets of $11.63 billion, most of which consisted of Ethereum and other digital assets.

Therefore, the balance sheet did not indicate an immediate solvency crisis. However, BitMine used $287.6 million in cash for operating activities in the first nine months of its fiscal year.

The company said legal, advisory, consulting and capital raising costs associated with the expansion of the ETH fund partially contributed to the outflow.

After the quarter, BitMine raised an additional $273.8 million by selling 3.5 million shares of BMNP stock, consisting of 9.5% perpetual preferred stock.

The offering not only strengthened the Company’s immediate liquidity but also introduced an annual preferred dividend obligation of approximately $33.25 million. Although the securities are stocks rather than ordinary debt, their higher status and higher dividend rates than common stocks add another recurring demand on BitMine’s resources.

Management said existing cash, projected operating cash flow, shelf registration and access to its ATM program should provide sufficient liquidity for at least the next 12 months.

That valuation depends in part on continued access to capital markets. If the price of Ethereum stagnates, BitMine’s stock price weakens, or investors become less receptive to additional issuance, the company may face higher funding costs or reduced flexibility.

BitMine’s latest filing thus presents two competing realities.

The company had built a staking operation that generated tens of millions of dollars in quarterly revenue and was able to cover its core operating expenses before changes in cryptocurrency valuations.

At the same time, option losses overwhelmed gains, long-term contracts added significant management costs, and the expansion of ETH’s treasury relied on equity issuance, more than doubling the number of shares outstanding.

BitMine’s long-term economics will therefore depend on whether staking income can continue to exceed treasury costs and option losses, whether the company can maintain access to capital, and whether Ethereum recovers enough to close the multibillion-dollar gap between the cost of its holdings and its market value.