Azad Engineering IPO Review – GMP and Everything You Need to Know

Azad Engineering IPO Review: Companies in the aerospace and defense industry have been welcomed in the stock market with large listing gains. Take the examples of MTAR Tech and Paras Defense. Both were listed and recorded rise rates of 77% and 180%, respectively. In this article on Azad Engineering IPO Review, we will take a look at the company, its finances, the key players in the market, and more.

In that sense, we would like to introduce you to another opportunity. Azad Engineering company is facing an IPO issue of Rs. 740 Cr will be released on December 20, 2023. The issue will close on December 22 and be listed on the exchange on December 28, 2023.

Azad Engineering IPO Review

About Us

Azad Engineering manufactures and supplies key components to original equipment manufacturers (OEMs) in the energy, aerospace, defense, and O&G sectors.

The company supplies various OEMs throughout the United States, China, Europe, Japan and the Middle East. Azad’s Marquee customers include: general electric, Honeywell International, Mitsubishi Heavy Industries, siemens energy, Eaton Aerospaceand MAN Energy Solutions SE.

Azad manufactures 3D rotating and fixture devices. Airfoil/blade section of turbine engine. This product applies to the following fields: gas, nuclear, and heat turbine. The Aerospace segment manufactures components for auxiliary power units, engines, and hydraulics for commercial and defense aircraft.

The company has four manufacturing facilities measuring approximately 20,000 square meters in Hyderabad, Telangana. Additionally, the company plans to add two additional manufacturing facilities totaling 1.7 million square meters.

As of FY23, Azad Engineering earned 87% of its revenue from the energy segment, specifically airfoils/blades. Aerospace & Defense accounted for 8.95% of revenue with Air Generation Systems accounting for the last portion of revenue. Oil and gas accounted for just 0.02% of revenue in FY23.

Industry introduction

The global energy turbine components market (accounting for 72% of the company’s revenue) was valued at Rs. 28,325 Cr in FY22 and is expected to reach Rs. The nuclear turbine market is expected to grow at a CAGR of 8%, with a size of 28,270 Cr in FY27, while the gas turbine market is expected to grow at 1% by 2027.

Additionally, the aerospace and defense components market was valued at Rs. 99,000 Cr in FY22 and is expected to reach 1.5 million Cr by FY27, growing at a CAGR of 9%. The overall market size of the company is expected to reach Rs. 1.81 million Cr by 2027.

India has traditionally had a foreign trade deficit. Over the past five years, our country’s exports have grown at a CAGR of 9%. The engineered products segment grew at a CAGR of 6.3% from FY18 to FY23.

Steel accounts for the largest share of total engineering exports, i.e. 22%. Industrial machinery, aircraft and spacecraft components account for 18% and 1% of engineering exports respectively, a niche market that Azad caters to.

The industry appears optimistic about new developments in India’s foreign trade policy in 2023 and several other initiatives of the government such as: Make in India, Atmanirbhar Bharat, and Production Linked Incentives (PLI).

Azad Engineering IPO Review – Financials

Azad reported a profit of Rs. 252 Cr in FY23, an increase of 29.42% from Rs. 194 Cr in FY 2022. Over the past three years, revenue growth has been very strong, with a CAGR of 43%.

However, net income failed to replicate the revenue trend. In FY23, the company reported a net profit of Rs 8.5 Cr, a 71% decline from Rs. 29 Cr in FY22. The sharp decline in net profit was due to an increase in financial costs of 5 million won. 52.3Cr or 21% of FY23 revenue.

It can be assumed that next year’s financial costs will have decreased significantly due to repayment of loans based on IPO net proceeds.

The company’s cash flow from operations (CFO) is Rs. -10.20 Cr in FY23 due to rapid increase in accounts receivable and inventory. CFO represents profits being converted to cash, and the FY23 numbers indicate a build-up of inventory and funds not yet received from vendors.

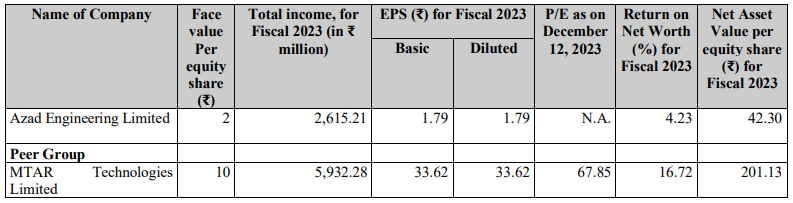

As of FY23, the company’s return on equity was 4.23%, return on capital employed was 12.99% and debt-to-equity ratio was 1.47x.

main players

When we compare Azad with its listed peers, we see that in terms of revenue, Azad is the second smallest on the list, right behind Paras Defense. In terms of earnings per share, Azad is the smallest company among its peers.

If you divide the stock’s maximum price by its earnings per share, you arrive at a whopping 292.73 times its price-earnings. This makes Azad the most overvalued stock.

However, as the company’s financial costs decrease due to early repayment of borrowings, PE valuation is expected to decline.

Company Strengths

- The Company operates in a highly engineered market where a zero-defect policy applies to some of the products it offers. This makes the company’s expertise in product manufacturing very important.

- According to Azad’s RHP, customer acquisition for the company takes place in four stages and can take up to 30 to 48 months. This long acquisition period increases the barrier to entry for competitors.

- The company is undergoing a large-scale expansion of its production capacity, fueled by internal accruals (retained earnings). This shows signs of strong demand that the company may want to accommodate.

- The company has long-standing relationships (over 10 years) with some of the most renowned global OEMs such as General Electric and Mitsubishi Heavy Industries.

company’s weaknesses

- The company derived 65% of its FY23 revenue from its top 10 customers, of which 33% came from its biggest spenders. This type of revenue stream creates concentration risk.

- Azad imports about 50% of its raw materials. The top three suppliers cost 50% of revenue, and the number one supplier costs 25% of revenue. Foreign currency fluctuations can have a significant impact on your profits.

- The company relies heavily on exports for 80% of its revenue in FY23 and 90% of its revenue in H1FY24. The company relies heavily on Japan and the United States, which generate 35.47% and 23.01% of its revenue respectively.

- In FY23, the company’s Net CFO fell into negative territory due to increased inventory and accounts receivable. This creates liquidity risk for the company.

Azad Engineering IPO Review – GMP

Shares of Azad Engineering Ltd were trading at a premium of 83.97% in the gray market on December 18, 2023. The stock in Gray Market was trading at Rs 964. This gives a premium of Rs 440 per share over the ceiling price of Rs 524.

Key IPO Information

promoter: Rakesh Chopra

Book Operations Lead Manager: Axis Capital Ltd, ICICI Securities Ltd, SBI Capital Markets Ltd and Anand Rathi Advisors Ltd

Proposal registered by: KFin technology company

purpose of the problem

- Of the net proceeds of Rs 138 Cr will be used to repay existing debt.

- Rs 60 Cr will be used as capital expenditure for purchase of plant and machinery.

- The remaining net proceeds will be used for general corporate purposes.

conclusion

As we conclude our article on Azad Engineering IPO Review, we have now come to the end of the article where we would like to briefly explain everything you need to know about the company and its IPO. The company has business interests in one of the most profitable industries in India. Each stock in this industry is valued at an average P/E ratio of 77x.

The company’s revenue growth appears fundamentally strong, but this growth rate has not (yet) translated into profitability. The weight of your debt will eat up a significant portion of your profits, and there will be times when you need a prepayment plan.

So what do you think about Azad Engineering? Can it really achieve a premium valuation at the same level as its peers? Let us know in the comments below.

Written by Nasir Hussein

by utilizing stock screener, stock heatmap, Backtesting Portfolioand stock comparison The tools on the Trade Brains portal give investors access to comprehensive tools to identify the best stocks, stock market newsBe aware and invest well.

Start your stock market journey now!

Want to learn stock market trading and investing? Check out exclusive stock market courses from FinGrad, a learning initiative from Trade Brains. You can sign up for free courses and webinars from FinGrad and start your trading career today. Sign up now!!

")