Aadhar Housing Finance IPO Review – GMP, Finance & More

Aadhar Housing Finance IPO Review: Aadhar Housing Finance is facing an IPO issue of Rs. 3000 Cr to be launched on May 8, 2024. The issue closes on May 10 and will be listed on the exchange on May 15, 2024. In this article, we analyze the GMP, financials, strengths and weaknesses of Aadhar Housing Finance IPO Review 2024. Read on to find out!

Aadhar Housing Finance IPO Review – Company Overview

Aadhar Housing Finance is a housing finance corporation focused on low-income housing segment disbursing loans amounting to Rs. 15 Lakhs. The company provides small-ticket loans to middle-class customers.

As of December 2023, total assets managed by the company are 50 billion won. 19,865 Cr. The average ticket size of a loan offered by Aadhar Housing Finance is Rs. 9-10 Lakhs, with an average loan-to-value ratio of 58.3% as of December 2023.

The company has a network of 487 branches, including 109 sales offices. 59% of the loans disbursed by HFC are to salaried customers and 41% to self-employed customers.

Note: If you want to learn candlestick and chart trading from scratch, here are some of the best books available on Amazon! Get the book now!

Since June 2019, BCP Topco has been the promoter of the company. BCP Topco is an affiliate of funds managed and advised by affiliates of Blackstone Group Inc “Blackstone”.

The company has secured funds from various sources including term loans, cash credit/working capital facilities. To meet its capital requirements, IR raises funds through issuance of NCDs, refinancing from the National Housing Board (NHB), and subordinated debt borrowings from banks, mutual funds and other domestic development agencies.

Aadhar Housing Finance has an experienced management team with an average age of 25 years in the financial services industry. The Board of Directors is comprised of outside directors and qualified and experienced personnel with extensive knowledge and understanding of the housing finance and banking industries.

Aadhar Housing Finance IPO Review – Industry Insights

Citing resilient domestic demand momentum, the International Monetary Fund (IMF) in its January 2024 economic outlook update revised India’s FY24 real economic growth estimate to 6.7 per cent in October 2023 from the previous estimate of 6.3 per cent.

Over the last three fiscal periods, the Indian economy has outperformed the global economy by growing faster. The IMF expects the Indian economy to remain strong and remain one of the fastest-growing economies in the future.

Improved financial literacy, increased mobile penetration, and the Prime Minister’s Jan Dhan Yojana bank accounts (a scheme to transition the unbanked to the formal banking system) have increased banking participation among non-metro individuals.

Demand for financial products in smaller cities has increased significantly in recent years as more people participate in the formal banking sector. Nonetheless, in terms of credit-to-GDP ratio, India has lower credit penetration compared to other developing countries such as China, indicating availability.

Similarly, in terms of household credit to GDP ratio, India also lags behind other markets. As of FY23, rural areas, which account for 47% of GDP, received only 8% of total bank credit. This demonstrates the vast market opportunity for banks and NBFCs to lend in this space.

As governments increase their focus on financial inclusion, increase financial awareness, and increase smartphone and internet penetration, the provision of credit services in rural areas will also increase.

Additionally, the use of alternative data for customer acquisition is expected to help financial institutions evaluate their customers and serve the informal sector of their communities.

Aadhar Housing Finance IPO Review – Finance

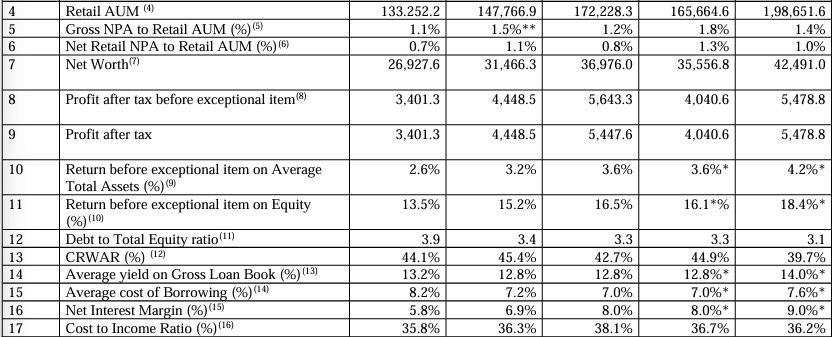

Aadhar Housing Finance’s FY23 interest income was Rs. 1776 Cr, up 15.5% from Rs. 1,538 Cr in FY22. Since FY21, interest income growth has maintained a CAGR of 12%.

Even though interest income growth was only 15.5% year-on-year, interest expense increased only 5% during the same period, with a CAGR of 1% since FY21.

Due to this reduction in borrowing costs, net interest income increased by 25.7% from Rs. 777 Cr in FY22 to Rs. FY23 has 977 Cr. HFC’s net profit also increased by 22.46% from Rs. 445 Cr in FY22 to Rs. 545 Cr in FY23.

HFC saw a 6.8% CAGR decline in live accounts from 2.56 Lakh in FY21 to 2.33 Lakh in FY23. This is due to a decrease in assets under management from 160 million won. 19,865 Cr in FY21 which is only Rs. 17,222 Cr in FY23. This was a financial highlight for Aadhar Home Finance. IPO examine

Also read…

Aadhar Housing Finance IPO Review – Key Players

Here’s a look at how Aadhar Housing Finance compares to some of its competitors listed in the market. Aadhar is the largest revenue generator among its peers, generating twice the revenue of the top two companies.

In terms of return on equity, aadhar also has the highest RONW at 16.5%, much higher than Aptus Value Housing Finance’s 16.1%.

Compared to its Aadhar HFC peers, TBO is offered at a higher issue price of Rs. 314 and basic income of Rs. 13.80 is issued at a PER of 22.75 times.

Company Strengths

- Focus on low-income housing sector: Aadhar Housing Finance focuses on the low-income housing market, which allows the company to leverage its presence across the majority of India’s population in towns and villages.

- Customer-centric business model: The company can provide loans to low-income and middle-class families who cannot obtain mortgage loans from regular financial institutions. This gives the company a competitive edge with the growing middle class.

- Extensive branch network: The company has a pan-India network of branches and sales offices. We have significantly increased our branch network from 310 in FY21 to over 487 as of FY23.

- Low non-performing assets: The company’s total non-performing assets stood at 1.2% in FY23. The Company has robust and comprehensive processes in place for underwriting, collecting and monitoring asset quality.

company’s weaknesses

- Pending lawsuits against former promoters: The company’s former promoters are under ongoing regulatory scrutiny by enforcement agencies, including the ED.

- Reliance on Third Party CRAs: The Company relies on information provided by the borrower and the respective credit rating agencies such as CRIF and CIBIL. Incorrect information provided by them may lead to non-performing loans being paid out.

- Risks of NPAs: As a Korea Housing Finance Corporation, our assets are loans paid to borrowers. HFCs expect to receive payments on a regular basis and there is a risk that payments will not be made by these borrowers.

- Lack of risk monitoring: Poorly managed HFCs lack the ability to monitor and manage risks, which can ultimately lead to non-performing loans that can negatively impact company profits.

Aadhar Housing Finance IPO Review – GMP

Shares of Aadhar Housing Finance were trading at a premium of 16.51% in the gray market on May 6, 2024. The stock in Gray Market was trading at Rs 367. This gives a premium of Rs 52 per share to the ceiling price of Rs 315.

Aadhar Housing Finance IPO Review – Key IPO Information

promoter: BCP TOPCO VII PTE.

Book Operations Lead Manager: ICICI Securities Ltd., Citigroup Global Markets India Pvt Ltd, Kotak Mahindra Capital Company Ltd, Nomura Financial Advisory & Securities (India) Pvt Ltd and SBI Capital Markets Ltd.

Proposal registered by: KFin technology company

purpose of the problem

- Rs 750 Cr will be utilized to fund capital requirements for future loans.

- The remaining amount will be utilized for general corporate purposes.

conclusion

Aadhar Housing Finance is a housing finance company focused on providing microloans to low- and middle-income earners. Key strengths include focus on underserved segments, extensive branch network, and relatively low NPAs.

However, the pending case against the former promoter and dependence on third parties are weaknesses. Financially, interest income and profits are steadily increasing thanks to the reduction in borrowing costs.

It is the largest revenue generator with the highest return on net assets compared to its peers. The price of this IPO is reasonable at a P/E of 22.75 times. Overall, it appears to be a promising opportunity considering its areas of focus and financials, but investors should consider the risks highlighted. So, would you like to invest in the upcoming IPO? Let us know in the comments below.

Written by Nasir Hussein

By leveraging the Stock Screener, Stock Heatmap, Portfolio Backtesting and Stock Comparison tools on the Trade Brains portal, investors have access to comprehensive tools to identify the best stocks, stay updated and informed with stock market news. invest.

Start your stock market journey now!

Want to learn stock market trading and investing? Check out exclusive stock market courses from FinGrad, a learning initiative from Trade Brains. You can sign up for free courses and webinars from FinGrad and start your trading career today. Sign up now!!

")