Bond markets portend potential short-term trading opportunities | “Filling the Gaps” with CMT

key

gist

- If Treasury yields move higher, sell the bear flag breakout and use the short-term decline as a selling opportunity.

- When yields are low, consider buying bull flags and setups.

- Yields are likely to be higher before a correction.

In our last article, we presented our long/term outlook for intermediate-term Treasuries, where we concluded that a structural break beyond the long-term downtrend from the September 1981 high was combined with a rise above the November 2018 pivot @ 3.25%. I took it down. Changed long-term long-term trend from low (bullish) to neutral. More work is needed to move the long-term trend from neutral to bearish. In this article, we will evaluate how weekly charts can interact with monthly charts, and then consider how investors might react to different scenarios set out over the coming weeks and months.

As a caveat, my analysis on shorter perspective time frames left no viable trades or even clear expectations of possible outcomes over the next few weeks. I think the market is ready to break out of the current congested area, and I think any direction out of this area will provide ample entry opportunities for short-term traders. This analysis allowed me to identify important chart points/zones to pay particular attention to behavior and market structure and define an appropriate trading plan.

10-Year Treasury Yield: Annual Perspective

The chart below shows the annual outlook for the 10-year Treasury note (INDX).

Chart 1: Annual chart of 10-year Treasury yields.

Note the break of the long-term downtrend and the upward move above the 3.35% pivot. It is worth noting that the Moving Average Convergence/Divergence (MACD) oscillator is on the rise for the first time since 1985.

Please note the following:

- The basic definition of an uptrend is a market that is consistently making higher highs and higher lows. For example, a good example of a downtrend can be seen in the annual 10-year Treasury chart, where yields have consistently made lower lows and lower highs for several decades, defining a very clear and unambiguous bull market (lower yields/higher prices). ).

- For bonds to begin to define a long-term weakness (falling bond prices/rising yields), yields must retreat from highs, define higher lows, and then achieve material new highs. From that point on, you can draw tentative annual and monthly trend lines and channel forecasts. You can also predict prices with Fibonacci and numbers. Importantly, this structure defines a long-term downtrend and places weekly and monthly momentum in harmony with annual momentum. I expect this transition to occur over the next 12 to 18 months.

- The big question in my mind is whether last October’s 4.98% high marked the end of the bearish structure that has been established since the 0.40% low. I think that’s true, and I think yields will come down by the middle of this year. However, there is also a reasonable case for a final rise into a stronger resistance area of around 5.25% followed by a reset, defining a higher low. Given this perspective, the development of the weekly charts over the next few months becomes particularly important.

10-Year Treasury Yield: Weekly Perspective

Below is a weekly chart of the US 10-year Treasury yield ($TNX).

Chart 2: Weekly chart of 10-year Treasury yields. Note the following points in the chart:

- Bonds typically build reliable channels and trend lines, but a move from 0.40% is unusual in that it is difficult to find a solid trend line or channel.

- We focus on the 2.52-3.25% (AB) trend line as the rise from the low does not provide a solid trend line or channel. Since last October, the decline from 4.98% has weakened repeatedly and the bounce from the trend line has been very modest.

- The inability of the trend line to generate selling (higher returns/lower prices) means that the pressure is not strong.

- A decline below the 3.79% pivot will likely extend back to the 3.25% pivot, with that area more likely around 2.65% (a retracement of about 1/2 the 0.40% to 4.98% move).

- An increase from 3.79% is generally seen as a bullish (low yield/high price) signal. Flags usually correct trends. Despite the extremely high volume experienced during the move to last October’s highs, volume during that period (as expected) declined significantly.

- One of my favorite patterns is the “Three Drives High and Low.” This chart may technically make sense (3.48% -> 4.33% -> 4.98%), but it hardly makes sense because the push to 3.48% is not proportional to the first two pushes. The chart is set for a final drive higher to potentially complete the sequence with strong resistance in the 5.25-5.35% area.

- We will also monitor the secondary test price of 4.98%. A completed secondary test would establish a significantly bullish (lower yields/higher prices) market.

The balance of structural evidence on the weekly chart favors lower yields, but this is a close situation and nothing special can be done at this level.

Looking at momentum

The multi-screen momentum perspective below is a quick filtering method I use. What’s important is that momentum is fractal (robust across time periods and markets). I prefer to derive trends through tape, so I only use the oscillator as a fast filter.

The chart below displays annual, monthly, weekly, and daily charts of the 10-year Treasury yield. On the chart, we return to returns.

Chart 3: Annual, monthly, weekly and daily charts of 10-year Treasury yields.

Important points to remember: Rising yields = falling prices.

- Year-to-date momentum has shifted towards higher returns/lower prices.

- Monthly momentum shifted towards lower yields/higher prices. A slight negative difference has formed, the monthly is at odds with the annual.

- Weekly momentum is mixed/neutral but trying to shift towards higher yields/lower prices. This struggle over the zero line suggests that action over the next few weeks is likely to define the direction of the next 25-50 basis points move.

Since I’m most interested in weekly trends (in ratios, the weekly perspective is most important), I usually follow the one trend higher. In this case, we are seeing signs of lower monthly returns and higher prices, and are just now moving into the MACD quadrant, where there is potential for a significant drop in returns. Weeks are also more likely to change into low returns/high prices to create harmony. But again the evidence is mixed. Sometimes you just need to let the price action unfold before making any firm conclusions.

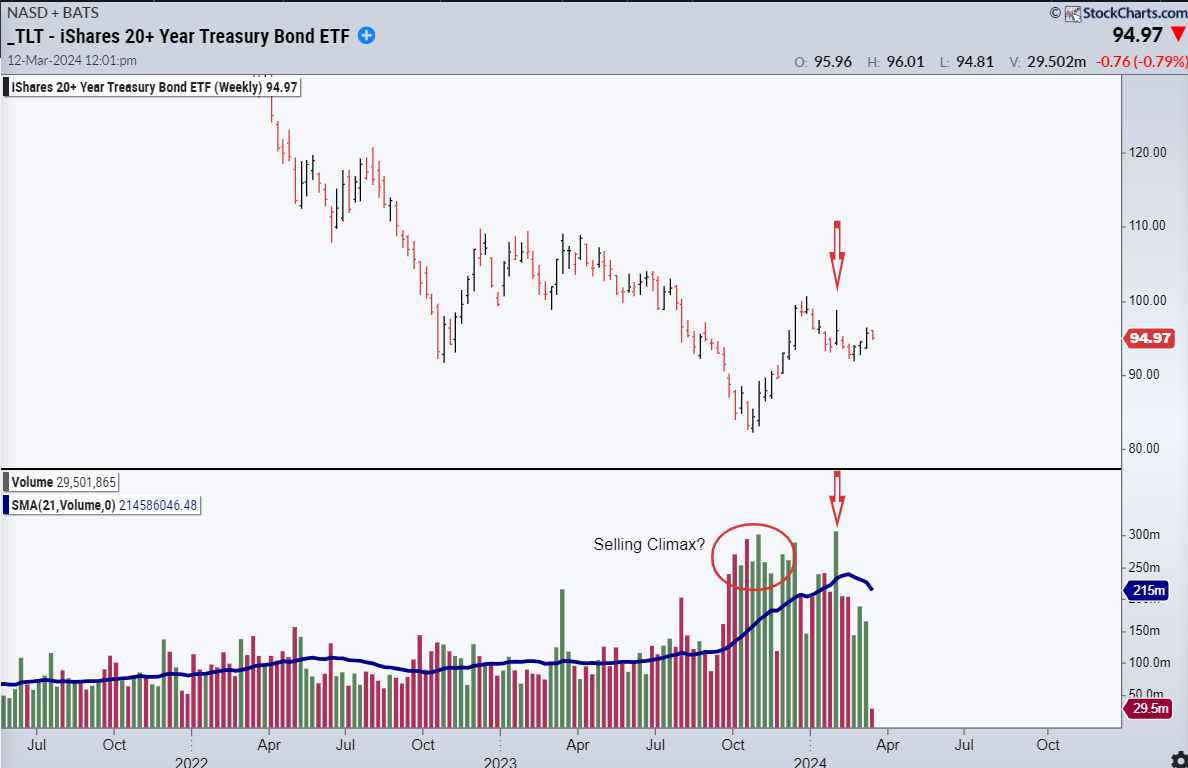

Weekly Perspective on Bond ETFs (TLT)

Some important points are: Volume:

- Since we are looking at the iShares 20+ Year Treasury Fund (TLT), we are looking at price (a downward trend is a bear market) rather than yield. This is because the yield indices we use do not have reported trading volumes. The caveat here is that in my professional capacity, I prefer futures volume. This is because futures trading volume is more representative of institutional interest rate investors, while TLT has a retail focus.

- Evidence between futures and ETF trading volumes is conflicting. TLT showed clear signs of short-term capitulation last October, but failed to produce a classic selling climax.

- Futures are more ambiguous with no apparent increase in volume, but the price action is more consistent with a selling climax.

- Since the October low, trading volume has remained fairly high overall and the rise has been relatively modest. The poor results relative to the effort expended suggest that the market continues to face high quality supply. The same price/volume relationship exists for futures.

- Notice that trading volume has dropped dramatically over the last 3-4 weeks as the market has risen. This is consistent with a bearish flag or pennant.

- Lastly, note the spike in volume (arrow) as sellers took to the market a few weeks ago. There are still strong sellers to power your bidding.

In my view, the balanced evidence suggests that the market peaked its selling in October. That peak is likely to last for most of this year, but it could be tested again.

10-Year Treasury Daily Yield

Chart 5: Daily chart of 10-year Treasury yield.

Please note the following:

- Seasonal trends. Yields tend to set a significant mid-year high early in the year and then fall towards mid-year. We are nearing the end of the bearish (rising yields/falling prices) annual period. This suggests a downtrend (lower returns/higher prices).

- Yields have struggled to break out of an upward trend (A/B), but have generally set up a bullish (rising prices/falling yields) flag. There is now pressure between internal resistance (gray side trendline) and AB channel bottom. From this perspective, weakness (higher yields/lower prices) is beneficial.

- If the market breaks higher in this area, where will resistance appear? With yields moving higher in this area, there isn’t much resistance between 3.50% and last year @4.89%. Above 4.89%, 5.25-5.35% is a reasonable target.

- There is a solid support confluence in the 3.23-3.30% area if the market declines from this area. However, the 0.50-0.618 retracement area of the 2.15-2.70% area is more likely to apply. This will likely be a result of the economic downturn.

conclusion

The next few weeks will be an important turning point on the daily and potentially weekly charts. The market has generally been consolidating over the past few months and a pattern breakout could be meaningful. For short-term traders, the direction of consolidation will likely define the direction of movement into the fall. In other words, we go together.

- As yields move higher, they will likely break through the bearish (falling prices/rising yields) flag and start selling, and they will view the short-term decline in yields as a selling opportunity. If it’s low, I’m likely to be a buyer of bullish flags and setups (falling yields/rising prices).

- If the market breaks away from the trendline at pace, the first solid support can be found in the 3.79% area.

- I do not see a small possibility that we will continue to see major weekly and monthly outlook adjustments (yields fall/prices rise) finally moving higher into the 5.25-5.50% area before eventually making higher lows. And while I think it would be advantageous to see generally strength (lower yields, higher prices) over the next few months, the analysis is provisional and the short-term benefit to the trade is minimal. In my trading, I consider them unviable without further price/volume development or reasonable structure to trade.

Out of respect for my macro work and business cycle work, I fully expect a severe recession to develop by the end of the year, so I will be a better buyer of bullish inflections on the weekly charts in the coming months.

disclaimer: Shared content and published charts are for informational and educational purposes only. CMT Association does not provide this information, and this information should not be understood or construed as financial advice or investment recommendations. The information provided is not a substitute for the advice of an investment professional. CMT Association will not be liable for any financial loss or damage that may occur to the audience.

Good deal.

Stuart Taylor, CMT

Certified Market Technician

Stewart Taylor retired from Eaton Vance Management in January 2020 after a 40-year career in U.S. fixed income with a focus on technical analysis and relative value investing. He joined Eaton Vance in 2005 as a senior trader on the investment grade fixed income team. During his tenure, he served as a portfolio manager for institutional separate accounts and mutual funds, managed the team’s inflation assets, and for a time served as the team’s strategist. Value, economic positioning. From 1992 to 2005, he provided private investment and trading advice to institutional buy-sides, broker-dealers, and hedge funds. Learn more