Fundamental analysis of Avalon technology

Fundamental analysis of Avalon technology: The Indian EMS market is expected to grow at a rapid CAGR of 32.3% to reach USD 80 billion by FY25-26. One such company in this space is Avalon Technology, which is different from the rest. Read this article to learn more about this company, its financials, and how it stands out compared to others.

Fundamental Analysis of Avalon Technologies – Company Overview

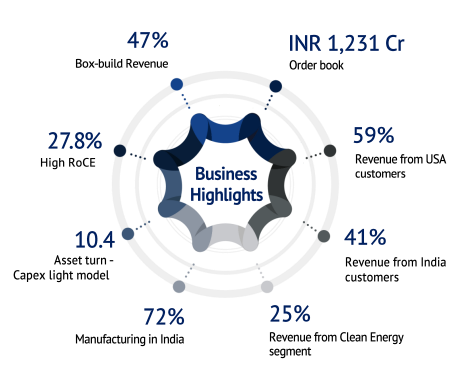

avalon technologyEstablished in 1999, the company is one of India’s leading fully integrated Electronic Manufacturing Services (EMS) companies and a major player in the Electronic Manufacturing Services (EMS) sector and boasts of 14 integrated and strategically located manufacturing units across the US and India. do. We have established ourselves as a leading EMS provider with a global presence through manufacturing, warehousing, and logistics.

With a diverse portfolio of products tailored to industries such as clean energy, transportation, industrial, communications and medical devices, Avalon serves as a one-stop destination for all your EMS needs.

Through its unique global delivery model, Avalon provides end-to-end solutions encompassing PCB design and assembly, cable assembly and wire harnessing, sheet metal fabrication and fabrication, magnetics, injection molded plastics, and complete box building services for electronic systems. .

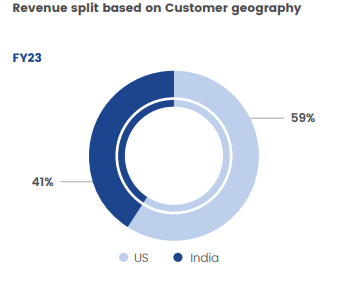

Unique among its Indian competitors, Avalon is the only EMS company with manufacturing facilities in the United States. The customer base extends to global OEMs in the US, China, Netherlands and Japan, reflecting Avalon’s reputation.

segment analysis

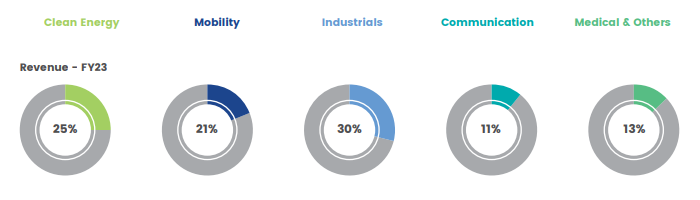

clean energy: Avalon operates core product lines in the clean energy field, including solar power, hydrogen, and electric vehicles (EV).

liquidity: Avalon works with customers in air, rail and automotive transport to create resilient and sustainable systems. We manufacture complex sheet metal processing, machining and injection molding plastics for aerospace applications.

Industrial goods: Avalon’s integrated design and manufacturing solutions help drive innovation across technologies such as power electronics and transformers.

Communication: Avalon supports 5G network equipment manufacturers through concept implementation and turnkey deployment. Integrated vertical manufacturing for our products enables our customers to use 5G technology.

Medical and other: The company supplies PCBA for oxygen concentrators, PCBA for blood analyzers, and cables for flow meters.

(Source: Annual Report)

Industry Overview

India continues to remain a bright spot in the global economic landscape. Drive sustained growth by leveraging demographic dividends, digital transformation, and innovation potential.

According to the Economic Survey, India’s GDP growth is expected to reach 6.5% in FY24, making it one of the fastest-growing economies, driven by a progressive regulatory environment, strong industrial policies, a deleveraging private sector and sustained capital expenditure.

The Indian EMS market is estimated to be worth $20 billion in fiscal 2021-22. The market is expected to grow rapidly at an average annual rate of 32.3% and reach $80 billion by FY25-26.

India’s electronics industry is recognized globally, especially for its research and development hubs, design and engineering services, and electronic systems design and manufacturing (ESDM) capabilities.

Also read…

Fundamental Analysis of Avalon Technologies – Finance

Sales and Net Profit

The company’s financial statements showed a 12% increase in revenue from FY22 to FY23 from ₹841 crore to ₹945 crore respectively. On a three-year CAGR, the company has grown by 10.15%.

The company’s net profit declined by 20% from ₹67 crores in FY22 to ₹53 crores in FY23. On a three-year CAGR, the company has grown by 45%. The decrease in net profit margin is because profits in the previous period increased due to profits generated from exceptional items.

The EMS industry is experiencing very favorable trends in India, which has resulted in a 43.5% increase in orders reaching Rs. 1,231 crores as on March 31, 2023, compared to Rs. $858 million as of March 31, 2022, providing greater revenue visibility in the medium term.

The table below shows Avalon’s sales and profits over the past four years.

profit

The financial institution reported an operating margin of 12% and net profit margin of 5% in FY23, compared to 12% and 8% in FY22. With a four-year outlook, the operating profit margin is 11% and the net profit margin is 4.5%.

Margins have continued to increase over the past few years as a result of careful selection, focus on integrated solutions with significant engineering content, and commitment to high-margin sectors such as aviation and clean energy. The decline in net profit margin this year is due to a decline in net profit.

The table below shows Avalon’s profit margins over the past four years.

rate of return

In terms of returns, Avalon’s business generates good returns on the capital employed and capital employed. RoCE and RoE in FY23 remained similar in size at 17% each, indicating efficient utilization of resources and good returns.

RoCE has maintained a stable level, and ROE has decreased compared to the previous year due to an increase in equity capital following the IPO. In the long term, the ratio has improved.

The table below shows Avalon’s ROE and RoCE over the past four years.

leverage ratio

If you look at the company’s leverage ratio, you can see that the debt-to-equity ratio has decreased. This indicates that the company is relying less on borrowed capital to finance its business and is able to retain more of its profits. Debt has decreased significantly compared to 3.37 times in FY22 due to repayment of loans from IPO funds.

The company’s interest coverage ratio has been strengthened, with FY23 ICR of 3.65x and the four-year average of 3x, meaning it can easily repay interest.

The table below shows Avalon’s D/E and interest coverage ratios over the past four years.

Fundamental Analysis of Avalon Technology – Key Indicators

Fundamental analysis of Avalon technology – future plans

- India in particular is at an inflection point, which is expected to expand India’s market share in the global EMS sector from 2.2% to 7% by 2026, creating tremendous opportunities.

- The company expects to double its revenue over the next three years and achieve solid revenue growth going forward.

- Avalon will maintain an optimal mix of customer base across India and the US to onboard high-value business from the US and execute it in India at a lower cost.

- The company plans to grow its traditional business by increasing wallet share through cross-selling and upselling.

- Avalon has begun expansion of its manufacturing plants, totaling approximately two square feet. 1.6 Lakh sq. in MEPZ-Chennai. ft. (mainly to be used in large box production)

conclusion

In the article “Fundamental Analysis of Avalon Technologies” we looked at Avalon Technologies’ business, its performance over the past four years, and its plans. The EMS sector currently has enormous opportunities in the world, with the fastest growing markets being India and the US, giving Avalon an additional advantage.

Additional analysis is required before investing to understand the risk and return characteristics of the company. What do you think about this company? We’d love to hear your thoughts in the comments section below.

Written by Ashish

by utilizing stock screener, inventory heatmap, Backtesting Portfolioand stock comparison The tools on the Trade Brains portal give investors access to comprehensive tools to identify the best stocks, stock market newsInvest well-informed.

Start your stock market journey now!

Want to learn stock market trading and investing? Check out exclusive stock market courses from FinGrad, a learning initiative from Trade Brains. You can sign up for free courses and webinars from FinGrad and start your trading career today. Sign up now!!