PepsiCo: Defensive, Steady Business With Long-Term Dividend Growth

Tim Boyle

PepsiCo, Inc. (NASDAQ:PEP) is an American multinational food, snack, and beverage corporation. Founded in 1898, PepsiCo is now a $232 billion (by market cap) food and beverage behemoth that employs nearly 320,000 people.

The company reports results across seven segments: PepsiCo Beverages North America, 30% of FY 2022 revenue; Frito-Lay North America, 27%; Europe, 15%; Latin America, 11%; Africa, Middle East, and South Asia, 7%; APAC (Asia Pacific), 6%; and Quaker Foods North America, 4%. The company generates approximately 57% of revenue from the US, whereas the remainder is generated internationally.

There are a number of reasons to be enthusiastic about this business and the opportunity for long-term investment. We’re talking about a simple-to-understand business model.

At its core, PepsiCo sells a variety of snacks and beverages (such as potato chips and sodas). But that’s greatly underselling it.

PepsiCo has been wildly successful at building, cultivating, and growing beloved consumer brands in snacks and beverages. In fact, PepsiCo has more than 20 different billion-dollar brands (i.e., brands that do more than $1 billion per year in sales). These brands include the likes of Aquafina, Doritos, Lay’s, Mountain Dew, and the eponymous Pepsi.

These food and beverage products are both consumable and low in ticket price, leading to a steady stream of repeat purchases by loyal consumers. And since the appeal of these products is timeless, that continuous demand stream can be relied upon.

Furthermore, because of the pricing power that PepsiCo commands through the strength of its brands, the company is able to slowly raise prices over time so as to keep up with, or even outpace, inflation. This combination has led to relentless business growth over the years, which has translated into relentless dividend growth.

Dividend Growth, Growth Rate, Payout Ratio and Yield

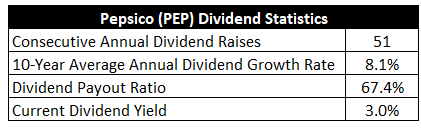

To that point, PepsiCo has increased its dividend for 51 consecutive years.

This is a Dividend Aristocrat and a Dividend King. It’s basically dividend royalty at this point.

The 10-year dividend growth rate is 8.1%. Not the highest growth rate out there, but this is a defensive, steady investment that one can sleep well at night with.

The odds of waking up to news that PepsiCo is suddenly in trouble are very, very low. And so one does, perhaps, sacrifice a bit of growth potential with that kind of easier, lower-risk setup.

On the other hand, with the stock yielding 3% right now, I think a high-single digit dividend growth rate is enough to get the job done here. This yield, by the way, is 30 basis points higher than its own five-year average.

With a payout ratio of 67.4%, based on TTM adjusted EPS, the dividend is protected and positioned for business-like growth. Simply put, the 50+ years of consistent dividend growth is almost certain to continue for many years to come. And that’s music to the ears of any long-term dividend growth investor.

Plus, anyone jumping on this legend today gets to kick that dividend growth journey off with a market-beating yield of 3%.

Great dividend metrics here.

Revenue and Earnings Growth

As great as these dividend metrics may be, though, they’re mostly looking backward. However, investors must always be looking forward, as the capital of today is being put on the line for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be extremely useful when the time comes to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top line and bottom line growth. And I’ll then reveal a professional prognostication for near-term profit growth. Blending the proven past with a future forecast in this way should give us the information we need to roughly gauge what the future growth path of the business could look like.

PepsiCo advanced its revenue from $66.4 billion in FY 2013 to $86.4 billion in FY 2022. That’s a compound annual growth rate of 3%. I’m typically looking for a mid-single digit top line growth rate from a mature business like this. PepsiCo falls a bit short, which is slightly disappointing.

However, I’ll just repeat that an investment in PepsiCo is more about steady, consistent compounding from a blue-chip business paying a steady dividend that’s consistently growing. One shouldn’t expect blowout growth here.

Meanwhile, earnings per share grew from $4.32 to $6.42 over this 10-year period, which is a CAGR of 4.5%. An 11% reduction in the outstanding share count, via repurchases over the years, helped to create this excess bottom line growth.

Notably, there’s a gap between GAAP earnings and adjusted earnings, so one can take their pick (using adjusted earnings for FY 2022 would show a higher 10-year CAGR). I’m using GAAP earnings here in order to create an apples-to-apples growth comparison.

To be honest, I’d prefer to see high-single digit bottom line growth here, even from a mature, blue-chip name like PepsiCo. Again, though, I think there’s something to be said for the safety of the business model.

Is that safety worth the lower growth in comparison to many other competing options in the market? That’s really an individual call.

All that said, we could have some good news on the growth front.

Looking forward, CFRA believes that PepsiCo will compound its EPS at an annual rate of 9% over the next three years. This would represent a material acceleration in bottom line growth (relative to what’s played out over the last decade). This seems like a reasonable assumption to make, in my view.

Much of the last decade’s growth has actually transpired over just the last few years, as PepsiCo really struggled to get moving for the first half of the last decade.

CFRA clearly sees this trend continuing, stating: “We expect (PepsiCo’s) net sales to rise by about 7% in 2023 and 5% in 2024, with ‘23 driven by 10% organic revenue growth. In 2022, (PepsiCo’s) net sales rose 8.7% due to organic revenue growth of 14.4%. We see organic sales growth driven by price increases as volumes have moderated in recent quarters.”

So that’s the top-line growth trajectory. But how do we get from there to the 9% bottom line number?

Well, CFRA sees margin expansion playing out: “We expect gross margin to expand by 120 bps in 2023 from the 2022 level of 53.0% as benefits from price increases and higher beverage volumes are partially offset by various cost pressures. (PepsiCo’s) on-premise beverage sales were hurt by Covid-19, but have since recovered.”

That’s really it. Above-average top line growth and some margin expansion gets us there.

If we agree with where CFRA is at on this, that sets up the dividend to remain in the high-single digit growth band it’s been in for the last decade. No huge assumptions need to be made for this to happen.

And being able to layer that kind of dividend growth on top of the 3% starting yield is a pretty compelling mix, especially when it’s coming from such a stalwart business.

Financial Position

Moving over to the balance sheet, PepsiCo has a good, but not great, financial position. The long-term debt/equity ratio is 2.1, while the interest coverage ratio is nearly 13.

The former number appears to be worse than it really is, due to abnormally low shareholders’ equity. I prefer to see low or no debt on a balance sheet, but PepsiCo’s situation here is not particularly concerning.

Profitability, on the other hand, is strong. Return on equity has averaged 61.8% over the last five years, while net margin has averaged 12.1%. ROE is juiced by the capital structure, but ROIC is routinely coming in at over 15%.

Fairly high returns on capital here. Overall, what I see is a blue-chip business that is as dominant as ever. And with economies of scale, a global distribution network, brand power, and established retail relationships with a large amount of shelf space, the company does benefit from durable competitive advantages.

Of course, there are risks to consider. Regulation, litigation, and competition are omnipresent risks in every industry.

Technology and the rise of alternative forms of media make it easier for new entrants to come to market, advertise, make themselves known to consumers, and compete with entrenched juggernauts like PepsiCo.

Trends toward healthier foods may negatively impact PepsiCo and many of its products that cater to taste appeal over health.

PepsiCo must continue to navigate different tastes in different markets, as well as changing consumer tastes and preferences.

The company’s international footprint exposes it to fluctuating currency exchange rates.

Input costs can be volatile. Passing on higher costs and raising prices on products can lead to strained relationships with retailers, as has recently been seen with certain retailers in Europe.

The balance sheet isn’t as strong and flexible as it used to be, which somewhat limits what management can do with capital allocation.

PepsiCo’s size may be a hindrance to future returns (i.e., the law of large numbers).

While these risks should be carefully thought over, the appeal of the business model and its brands should also be weighed. Also, with the stock down 15% from all-time highs, the appealing valuation is worth thinking over…

Stock Price Valuation

The stock is trading hands for a P/E ratio of 22.2. That’s based on TTM adjusted EPS, if only because of so many adjustments to EPS recently. I don’t see that as terribly high for a world-class business with some of the world’s most successful consumer brands.

The current sales multiple of 2.5, which is also not all that high, compares favorably to its own five-year average of 2.8. And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis. I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

Arguably, this is a pretty conservative take. My number is slightly below the demonstrated dividend growth rate over the last decade, and it’s quite a bit lower than the near-term forecast for EPS growth.

However, I think it’s worth acknowledging the stunted, mid-single digit EPS growth over the last decade, maturity of the business, elevated payout ratio, and stretching balance sheet.

It’s quite possible that PepsiCo grows the dividend at a rate that exceeds this level over the coming years. But I’d rather err on the side of caution and be pleasantly surprised to the upside.

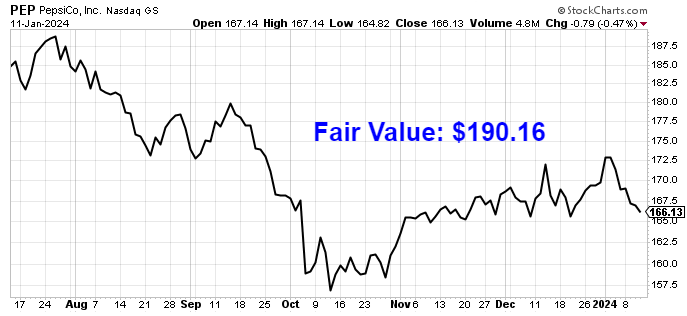

The DDM analysis gives me a fair value of $180.47. The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth. It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today. I find it to be a fairly accurate way to value dividend growth stocks.

I believe my valuation model was fair, if conservative, yet the stock comes out looking decently cheap anyway. But we’ll now compare that valuation with where two professional stock analysis firms have come out at. This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system. 1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value. Morningstar rates PEP as a 4-star stock, with a fair value estimate of $180.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line. They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold. CFRA rates PEP as a 5-star “Strong Buy”, with a 12-month target price of $210.00.

Boy, I landed very close to where Morningstar is at on this one. Averaging the three numbers out gives us a final valuation of $190.16, which would indicate the stock is possibly 12% undervalued.

Bottom line

PepsiCo, Inc. is a world-class, dominant, blue-chip business with more than 20 different billion-dollar brands. By selling low-ticket, tasty items with timeless appeal, the company has cultivated loyal customers all over the world. With a market-beating yield, a high-single digit dividend growth rate, a reasonable payout ratio, more than 50 consecutive years of dividend increases, and the potential that shares are 12% undervalued, long-term dividend growth investors looking for defensive stability should take a close look at this Dividend King.

Disclosure: I’m long PEP.

Note from D&I: How safe is PEP’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 93. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, PEP’s dividend appears Very Safe with a very unlikely risk of being cut.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

")