What goes up may not come down, but the Sharpe ratio is low

Buena Vista Pictures

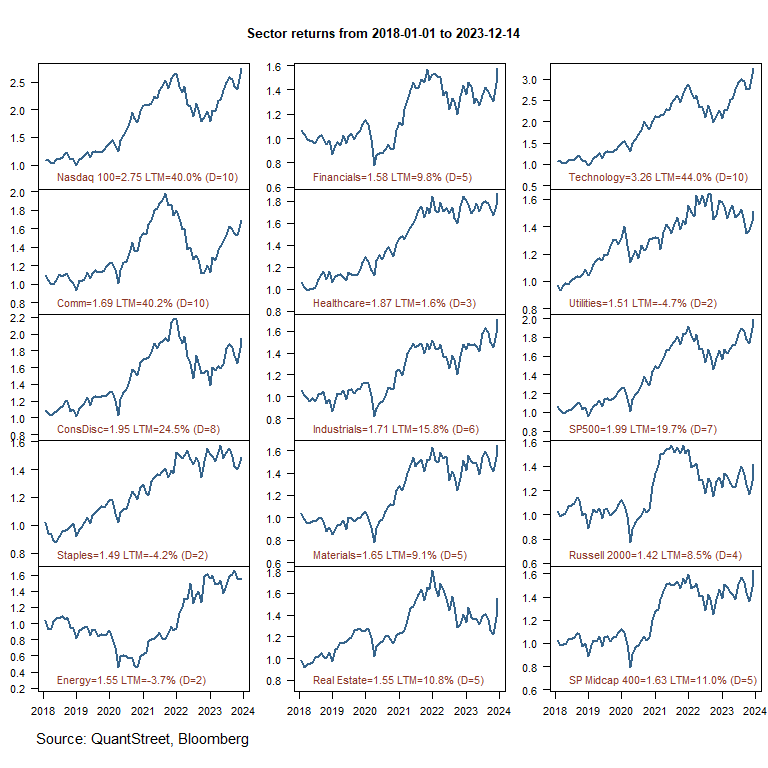

As I wrote recently, falling inflation and slowing growth, evident over the past few months, provide a good backdrop for risk assets. So good, in fact, that the entire stock market and some sectors, such as technology, are hovering near or near it. It reached an all-time high. Technology catalysts are well known, including excitement about AI, work-from-home trends, and strong profitability. The following chart shows the returns of U.S. stock market sectors over the past six years. Last 12 months (LTM) returns are shown in the legend along with the return decile to which the LTM returns fall.

Deciles are calculated using sector-specific observations in monthly rolling windows since 1990. Decile 10 (D=10) means that the LTM return for that sector was higher than 90% of all sector-specific observations (i.e., for one sector in the past year). Over 30 years. Decile 5 (D=5) means that LTM returns are higher than 40% of all sectoral return observations in the sample. The number to the right of the sector name represents the value of each dollar invested in that sector at the beginning of 2018. (Quant Street, Bloomberg)

The three best-performing sectors in 2023 were the Nasdaq 100, technology, and communications. All three are up more than 40% from before, driven by strong performance by large tech stocks. 12 months. Based on this LTM performance, the three indices are in the top decile of the sectoral return distribution (i.e., above 90% of all previous sectoral return observations). There can always be concern that after a period of such extreme performance, future earnings prospects may become bleak.

boom of the past

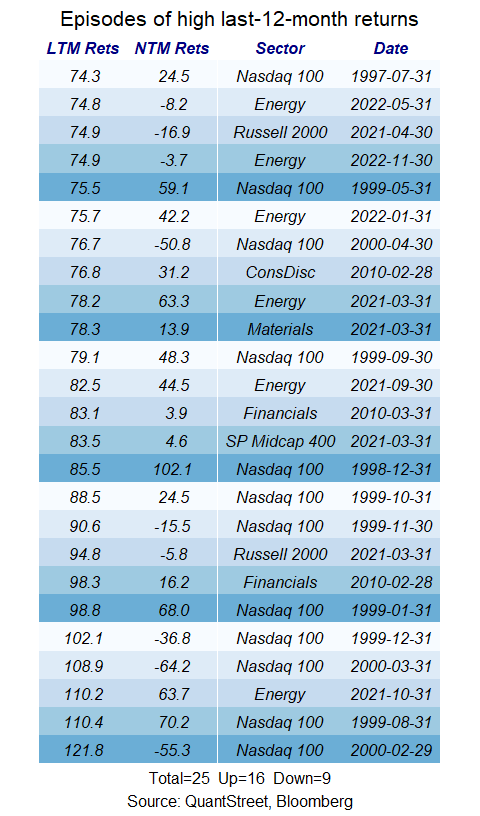

However, the mere fact that certain sectors of the stock market have posted strong year-over-year returns is not in itself a reason for pessimism. The following table shows the highest returns by sector year-over-year using data from 1990 to the present. that much LTM Court Columns display sector returns over the last 12 months. NTM rare The column shows returns over the subsequent 12 months. The date corresponds to the last month of that date. LTM Court calculate. For example, the energy sector’s return for the 12 months ending January 31, 2022 was 75.7%. It then recorded an additional return of 42.2% over the subsequent period. 12 months.

Quant Street, Bloomberg

In fact, 16 of the 25 highest annual sector returns since 1990 saw further gains in the following year. Although only 9 out of 12 months had losses, some of the losses were significant. Additionally, many of the most negative sector return observations are associated with overlapping 12-month periods during the bursting of the dot-com bubble in late 1999 and early 2000. That is, it is not an independent event, but reflects one specific selling episode. (For completeness, a list of the 25 sector-specific events with the lowest LTM returns is presented at the bottom of the article.)

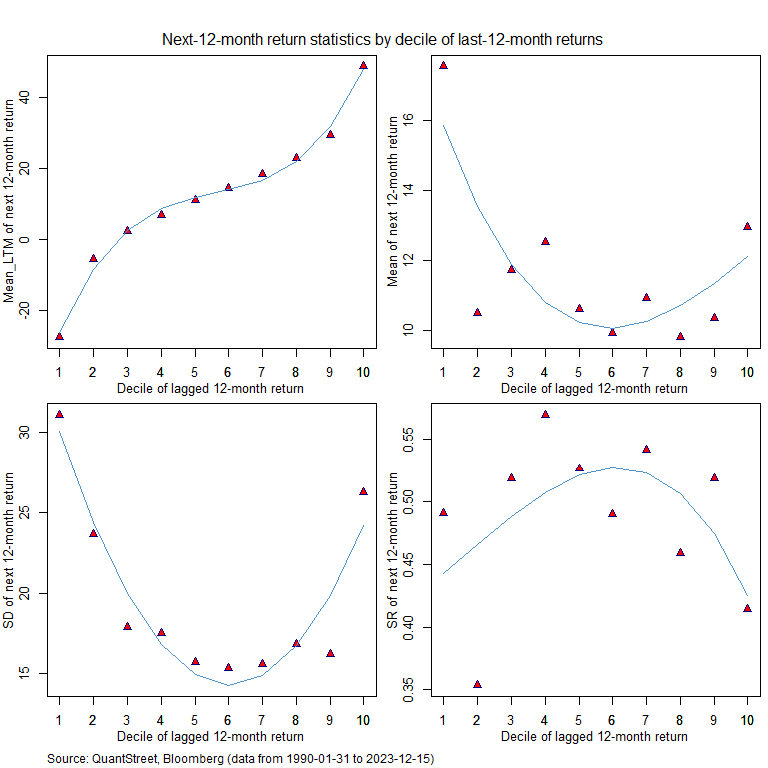

To gain more insight into market behavior following large sector rallies, we now group LTM sector returns into decile intervals based on past performance. The first decile contains the lowest LTM segment returns, and the tenth decile contains the highest LTM segment returns. The top left panel of the following figure shows the average LTM return for each bin. The average LTM return in decile 1 is -28%, and the average LTM return in decile 10 is 49%. LTM returns increase monotonically across intervals for each configuration.

Triangles correspond to bin-level return statistics. The blue line is The best fitting cubic polynomial is displayed to highlight the overall pattern. The Sharpe ratio shown in the bottom right is the average of: The 12-month return equal to or greater than the yield on short-term Treasury securities (excess yield) divided by the volatility of the excess yield. (Quant Street, Bloomberg)

The top right panel of the picture shows what happens next. 12 months after LTM returns in each decile. Interestingly, for the worst past results, the average The 12-month return is very positive at 20%. This then falls to the 10%-12% range for the next eight bins, rising to 13% for bin 10. That is, sector observations in the top decile of LTM returns, on average, lead to the next step. The 12-month return is +13%, which is higher than the results for all bins except the first decile. What goes up does not necessarily come back down.

But not everything is rosy. The bottom left panel shows the following volatility: This is the 12-month return for each decile. Volatility of: The 12-month returns show a clear U-shaped pattern. The extreme bins based on LTM returns represent the next highest volatility. This is the 12-month return result. The first decile (past bust) has the highest forward volatility at 31%, while the top decile (past boom) has the second highest forward volatility at 26%. Bins 3 to 9 have much lower future volatility, ranging from 15% to 18% (whereas bin 2 still has high return volatility). Higher average returns in Bins 1 and 10 are associated with much higher future volatility.

To evaluate the risk-return trade-off of each LTM return bucket, the following Sharpe ratios are displayed in the bottom right panel: 12 months returns. This is calculated as the average excess return for each sector over the next period, i.e. the return that exceeds short-term Treasury yields. 12 months divided by the volatility of excess returns. Except for Bin 2 (which is likely a statistical coincidence), the Sharpe ratios show a distinct hump-shaped pattern. The highest Sharpe ratios occur in the middle range, where returns are not too high and volatility is not too high. The bust section (decile 10) has a relatively low Sharpe ratio of 0.49, and the boom section (decile 10) has the second lowest Sharpe ratio of 0.41. Next highest average bins 1 and 10 12-month returns are very volatile and the effect is so dominant that the extreme bin Sharpe ratios are lower than the intermediate bin ratios.

scope of results

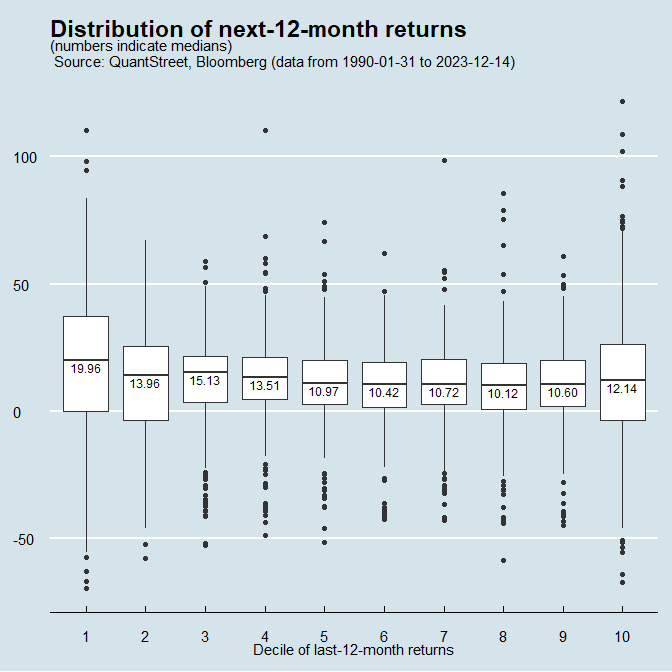

To better understand the distribution of future return outcomes for each LTM return box, the following chart displays a box and whisker plot of the next 12-month returns for each decile box. The horizontal line in each box represents the median: 12-month results for each decile interval. This has a similar shape to the average return shown in the previous figure. The height of each box, i.e. the vertical distance from top to bottom, represents half of all results between the 25th and 75th percentiles of the next item. 12 months returns. The vertical lines extending from the top and bottom of each box are 1.5 times the height of the box. And the points at the top and bottom of each decile represent the following extreme outliers: This is the 12-month profit from each bucket.

Quant Street, Bloomberg

For example, for bin 1 the median is The 12-month rate of return is 19.96%. The 25th to 75th percentile results range from 0% to approximately 40%. The next most extreme positive thing. The 12-month return is +110%, with the most extreme negative return being -70%. For Bin 10, these two extreme values are +122% and -67%, respectively. The box and whisker plot reinforces the message of Sharpe ratio analysis. Extreme bins have a very wide range of possible future outcomes, and the volatility they cause is so high that the Sharpe ratio is Even though the next mean is higher, the 12-month returns for the extreme bins are lower than those for the middle bins. 12 months returns.

looking ahead

With the caveat that the past is no guarantee of the future, my analysis of extreme returns suggests that just because technology stocks have had a big rally over the past year doesn’t necessarily mean they’re in for a big correction. In fact, the average returns for industries that experienced similar booms in the past were significantly higher. At the same time, the volatility of one-year forward returns for these booming sectors has been very high, with some producing very positive results and others extremely negative.

QuantStreet evaluates: It shows the 12-month returns for an asset class using two indicators: the results of a machine learning forecasting model and the last indicator. 12 month return trend. According to the former (machine learning model), tech stocks are not looking very good. According to the latter (trend), technology stocks look very attractive. Mixed signals from models and trends make tech stocks look attractive. The current findings do not question this analysis, but they do offer some cautions about the near future of the technology sector. This means that average returns are high, but volatility is very high and there is the potential for extreme negative and positive movements.

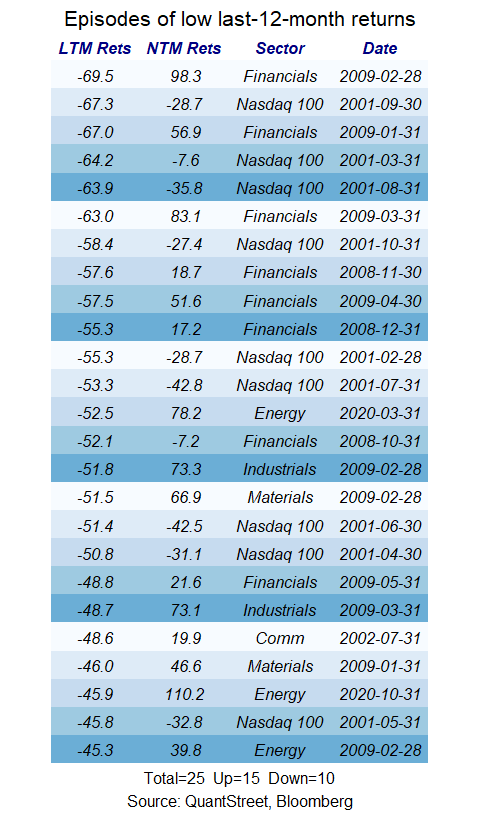

bust of the past

For completeness, the table below lists the 25 largest year-over-year declines across various sectors.

Quant Street, Boomberg