Fatal flaw in modern monetary theory

The following is an excerpt from the latest edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be the first to get these insights and other on-chain Bitcoin market analysis delivered to your inbox, Subscribe now.

Modern Monetary Theory (MMT) is receiving attention again with a new movie. find money A recent clip that went viral on Bitcoin Twitter and Fintwit. In the video, Jared Bernstein, Chairman of the President’s Council of Economic Advisers, is shown failing to explain the most basic concepts about government debt and money printing. He claims MMT is accurate, but some of the language and concepts (the most basic ones) confuse him. Considering his role, this is a truly shocking statement.

In this article, I will describe some key flaws in MMT that you, the reader, can use to debunk MMT. As Mr. Bernstein illustrates, the stakes are high as MMT cultists hold power in governments around the world. Putting these people in power is a very dangerous proposition. Because they will rapidly destroy the currency and cause economic Armageddon. As Bitcoin users, we believe Bitcoin will replace the credit-based dollar, but we hope the transition will be natural and relatively smooth. A major currency collapse without Bitcoin ready to take the lead would be disastrous for many.

Introduction to MMT

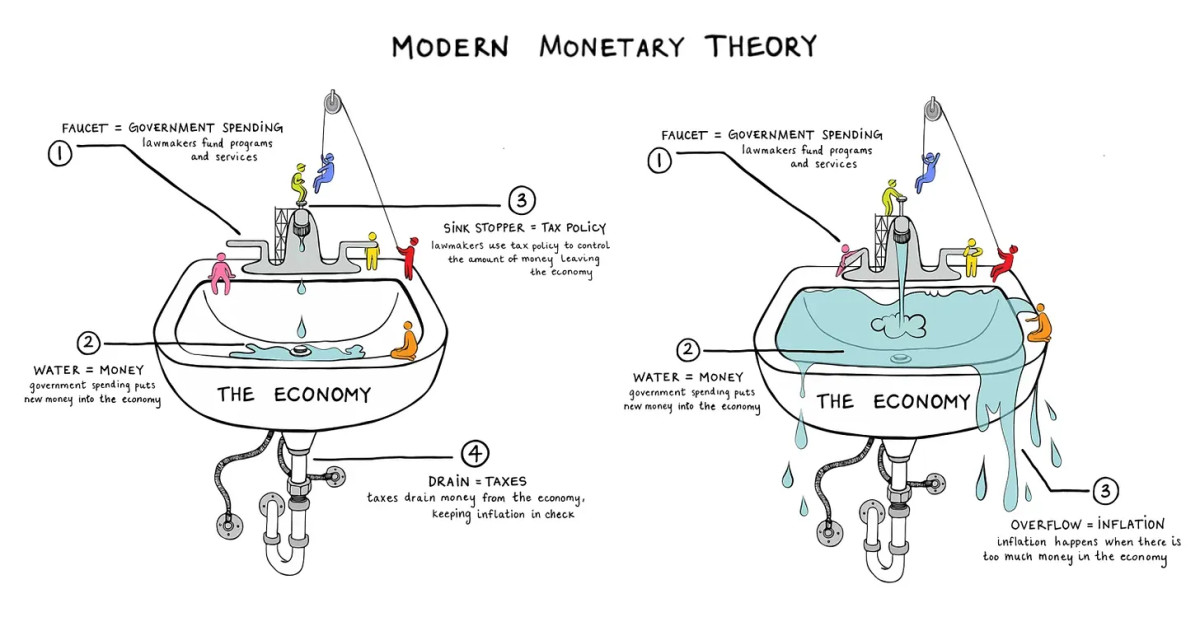

Modern Monetary Theory (MMT) is a post-Keynesian macroeconomic theory that argues that fiscal deficits are not inherently important, monetary policy should be subordinated to fiscal policy, and monetary authorities should issue primary money to finance large government programs. It is an economic framework. MMT promises to eradicate involuntary unemployment and solve social problems such as poverty and climate change. MMT is rooted in the belief that all money is a creation of the state and is designed through a legal framework to facilitate government control of economic activity.

According to MMT, a government that can issue money at will cannot go bankrupt. However, this power has obvious limitations, such as the inability to control the value of money. MMT also redefines the traditional functions of money, such as medium of exchange, store of value, and unit of account, arguing that these functions are merely by-products of government policy rather than intrinsic properties such as scarcity and divisibility. This theory leads to the controversial notion that governments can designate any item – acorns, IOUs, Bitcoin, etc. – as money based solely on legal declarations, ignoring their properties, which is completely at odds with actual economic dynamics. Concept.

No consistent theory of value

The most important shortcoming of modern monetary theory is its approach to the theory of value. Instead of a subjective theory of value in which prices emerge through the preferences of individual agents, such as personal spending or savings decisions, MMT replaces this with a democratic or collective theory of value.

According to MMT, the value of money is not derived from its utility as a medium of exchange, store of value, or unit of account. Instead, in MMT, the value of money comes from collective acceptance and trust in the country that issues it. This acceptance supposedly gives value to money. In other words, MMT turns the traditional understanding on its head. Something of value becomes valuable not because it is accepted as money, but because it is forced to be accepted as money.

The value of a currency depends on the state acting as a kind of economic calculator rather than on individual market actors. The aggregate preferences of society along with central planning expertise enter the equation and full employment is the result. This is no joke. They have no theory of value beyond what has just been described.

Mechanisms of MMT: Taxes and Fiscal Policy

Modern Monetary Theory presents a distorted understanding of fiscal policy and taxation, suggesting that taxes serve as a base load for demand for government-issued funds. Without taxes, MMT supporters argue, government spending would lead to devaluation. This point presents a notable contradiction. MMT adherents fervently deny that deficits matter at all while insisting that taxes are essential to offset their negative effects.

Moreover, MMT believers overlook the broader dynamics of currency markets. Taxes alone do not necessarily stimulate demand for holding currency. Fear of depreciation may lead individuals to minimize their holdings and convert other assets into cash only when necessary to meet their tax obligations. For example, an individual may acquire only the amount of domestic currency necessary to operate and pay taxes primarily using the alternative currency.

In terms of fiscal policy, MMT argues that the main constraint on money printing is inflation, which is due to the availability of real resources such as labor and capital. In their ideology, printing money causes economic growth until labor and capital are fully employed. Raising taxes is a mechanism to fight inflation by taking money out of the economy.

Another important flaw of MMT is that it requires belief that the state can accurately manage the outcomes of its fiscal policies. MMT overlooks the inherent limitations of central planning, particularly its assumption of perfect policy transmission without actual market data or evaluation of external market dynamics, and its circular reasoning that information guiding fiscal policy is merely a reflection of previous government actions. . Are MMT planners in control? Then it is circular. If not, it’s wrong.

MMT requires frequent policy adjustments and does not acknowledge the existence of unintended consequences that weaken demand for the currency. Because that means they have no control. Moreover, market interest rates further complicate matters for MMT believers. Micromanaging the economy leads to sharp declines in economic activity, lower demand for currency, and higher interest rates. As a result, MMT asserts that while a country can dictate the use of its currency, it has no power to control how markets value or trust that currency.

MMT and resource allocation

MMT’s approach to resource allocation emphasizes achieving “full employment” through top-down fiscal policy without considering the efficiency of labor and capital use. Proponents of MMT argue that sound fiscal policy can ensure full employment of labor, capital, and resources. But they try to use MMT principles to justify why seemingly unproductive activities, like digging holes and refilling them, are less beneficial than market-derived employment of labor and capital. This often leads to vague explanations for differences in production without clear and consistent value criteria.

According to MMT, all economic activities that consume the same resources should be recognized as having equal value, and the lines between productive investment and wasteful spending should be blurred. For example, there is no fundamental difference between using resources to build essential infrastructure and building a “bridge to nowhere.” This lack of understanding of value leads to policies that make employment the primary goal rather than the value created through employment. The result is a gross misallocation of labor and capital.

Conclusion and Implications

The basic principles and policy implications of Modern Monetary Theory are seriously flawed. These range from inconsistent theories of value and reliance on circular fiscal policy logic to failures in competitive international currency markets and unworkable resource allocation strategies. Each of these risks could have serious consequences if MMT is widely implemented.

For those following the Bitcoin space, the similarities between MMT and central bank digital currencies (CBDCs) are particularly striking. CBDC represents a transition from the current credit-based monetary system to a new form of fiat currency that can be tightly controlled through programmable policies. This reflects MMT’s advocacy for pure fiat money governed by detailed fiscal policies. This alignment suggests that regions such as Europe and China, which are making progress in implementing CBDCs, may naturally gravitate to MMT principles.

This transition is monumental. Regardless of what MMT fanatics would like you to think, no major economy can immediately convert to a new form of fiat currency. The transition will take place over several years, during which time we will witness the decline of traditional currencies. As MMT and these governments unintentionally champion Bitcoin, the choices for individuals, capital, and innovators will become clear. If people were to adopt an entirely new form of money anyway, it would be a simple choice for capital, economic activity, and innovation to flee to Bitcoin.